Perhaps you have heard a popular story from the investing world claiming that the best investment results are achieved by… investors who have died. In various versions of this story, there is a supposed study by a large brokerage firm which, after analyzing the performance of client accounts, discovered that the highest returns were generated by accounts belonging to deceased clients or those who had simply forgotten about their accounts.

The explanation was simple:

- the owners of these accounts did not trade,

- did not react to market emotions,

- and did not make impulsive decisions.

This story is often repeated in investing books and blogs. The problem is that when you try to find the original study, it turns out to be more of an internet legend than a well-documented fact.

That does not mean, however, that there is no truth behind the story. On the contrary, many reliable studies show that the majority of individual investors underperform the market. Interestingly, the main reason for this gap is usually not fees, lack of knowledge, or inadequate tools. The biggest problem turns out to be… the investor. More precisely – their cognitive biases and emotions.

Before I explain what this means, let me first share a few research findings.

Individual Investors vs. the Market

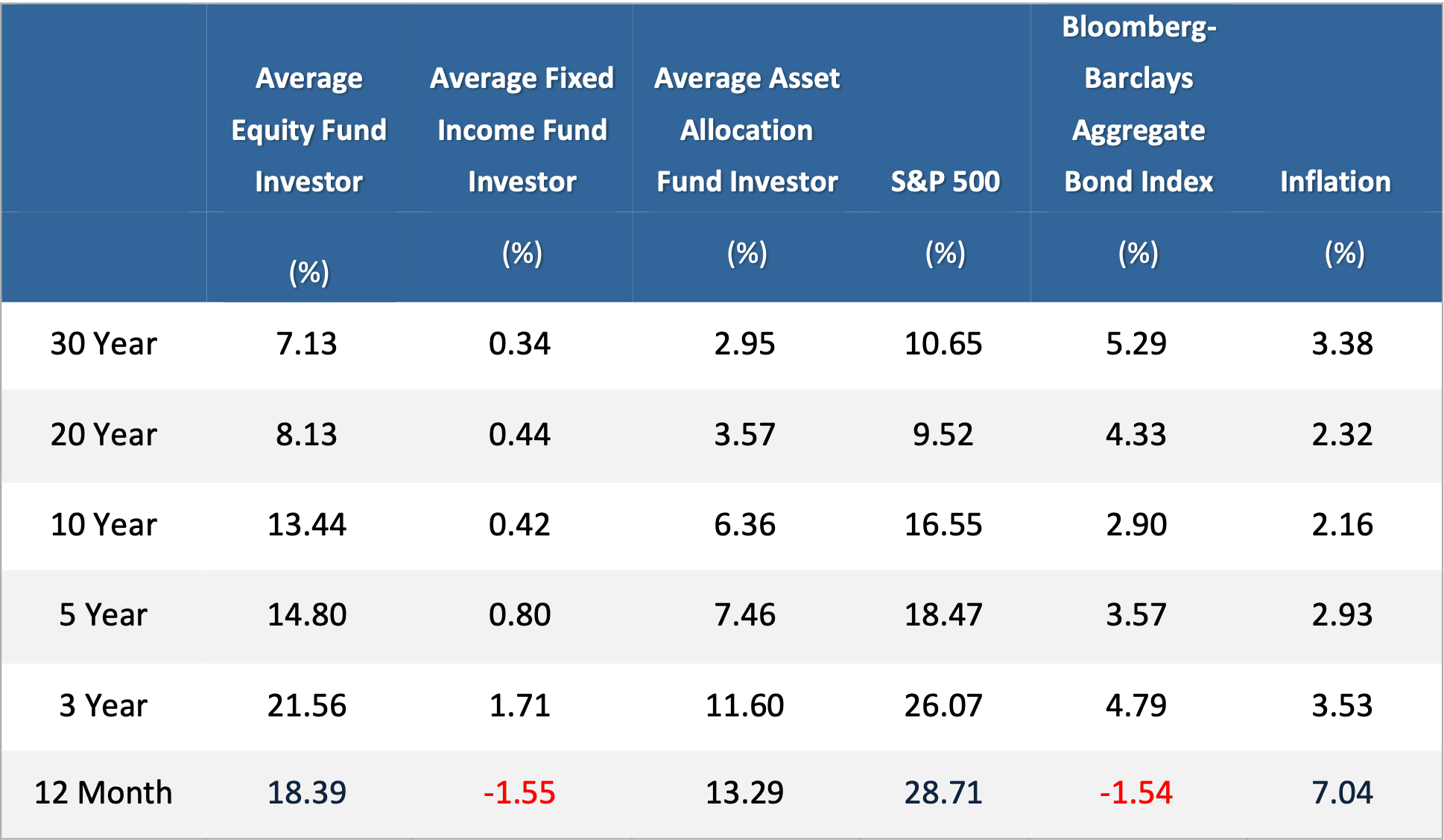

The Quantitative Analysis of Investor Behavior 2022 Study

One of the most widely cited studies showing how individual investors perform relative to the market is the report “Quantitative Analysis of Investor Behavior 2022” prepared by DALBAR, which analyzes the actual behavior of investors. The study covers the period 1985–2021 and shows that the average investor consistently underperforms the market itself. For example, over a 30-year horizon, the average investor in equity mutual funds earned 7.13% annually, while the S&P 500 delivered 10.65% per year. A similar pattern can also be observed in fixed income funds, where investors likewise tend to achieve lower returns than the market benchmarks. This illustrates the scale of the so-called investor return gap — the difference between market performance and the actual returns achieved by investors. You can see this in the table below.

Table 1. Average investor vs. market returns (DALBAR QAIB, 1985–2021)

The primary cause of this gap is not the investments themselves, but investor behavior. Influenced by emotions, investors tend to sell and buy their assets at particularly unfortunate moments.

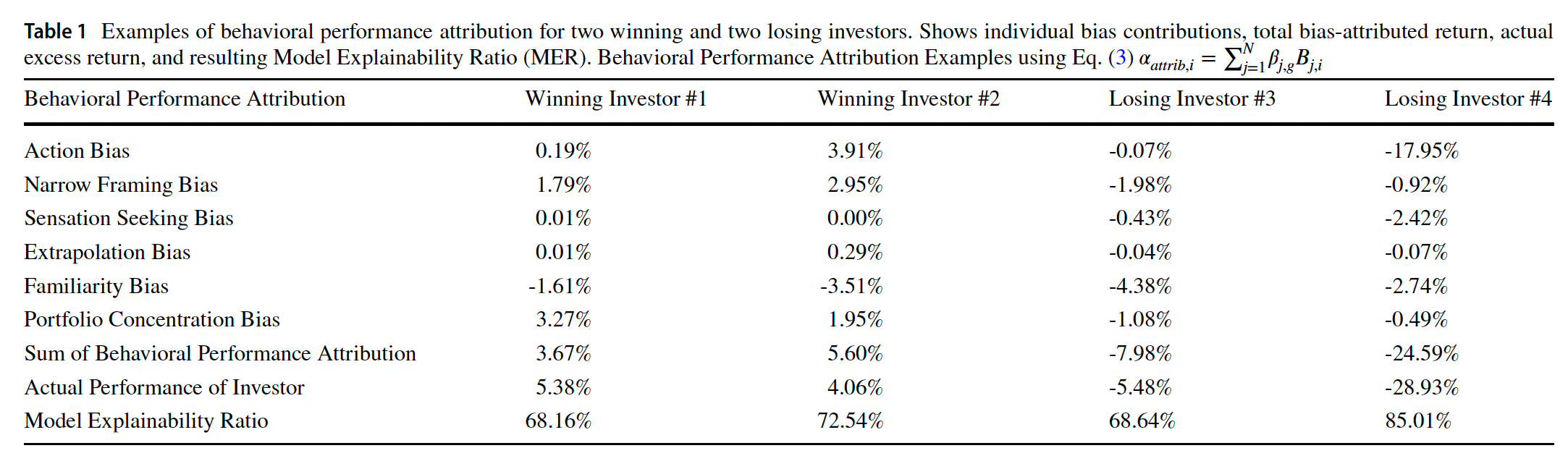

Study: Behavioral Performance Attribution of Retail Investors’ Portfolio Returns

Similar conclusions come from the study “Behavioral Performance Attribution of Retail Investors’ Portfolio Returns” conducted by David Gorzon and Rüdiger von Nitzsch from RWTH Aachen University. The authors analyzed data from 20,000 individual investors in Germany covering the period 2018–2023, including actual transactions and portfolio performance.

The results showed that only about 25% of investors outperformed the benchmark, while roughly 75% underperformed the market, represented by MSCI World.

The study also demonstrates that a significant part of these outcomes can be explained by investors’ behavioral biases.

Among the most important are:

- excessive trading activity (frequent transactions),

- portfolio concentration in a small number of stocks,

- chasing highly volatile assets,

- and a tendency to favor familiar, local companies.

For readers who want to explore the topic further, the impact of individual cognitive biases on investor performance is presented in the table below, which summarizes the study’s findings.

Table 2. Examples of behavioral performance attribution for two winning and two losing investors, showing individual bias contributions, total bias‑attributed return, actual excess return and the resulting Model Explainability Ratio (MER), based on Gorzon & von Nitzsch (2025).

Study: Most Vanguard IRA Investors Shot Par by Staying the Course: 2008–2012

Another study offering valuable insight is “Most Vanguard IRA Investors Shot Par by Staying the Course: 2008–2012”, prepared by Stephen M. Weber from the Vanguard Center for Retirement Research.

The analysis used data from 58,168 self-directed IRA retirement accounts held at Vanguard over the period 2008–2012. Researchers compared the investors’ actual results with two benchmarks based on simple investment strategies. The results showed that the average investor achieved returns close to the benchmarks, but those who actively changed their portfolios performed noticeably worse.

Investors who made at least one fund exchange during the analyzed period earned returns that were on average 1.04 percentage points per year lower than the asset allocation benchmark. In contrast, investors who made no such changes achieved results close to the benchmarks or even slightly better.

The study therefore suggests that the main source of weaker investment performance is not the investments themselves, but the decisions made by investors, particularly attempts to react to market events and frequent portfolio changes.

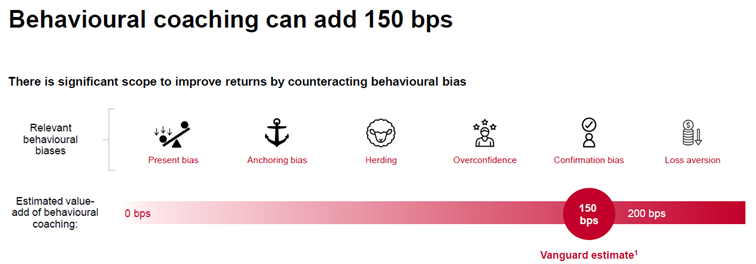

Even Vanguard emphasizes this point in its material for financial advisors on behavioral coaching (Vanguard’s Adviser Guide to Behavioral Coaching, 2024). The firm highlights that a substantial part of investment outcomes depends not on asset selection but on investor behavior.

Within its concept of Adviser’s Alpha (the value added by an advisor) Vanguard estimates that a well-structured advisory process can improve an investor’s long-term returns by up to about 3 percentage points per year. Importantly, around 1.5 percentage points of that advantage comes from reducing behavioral mistakes, such as attempts to time the market, chasing fashionable investments, or reacting to short-term market volatility.

Figure 1. Vanguard’s estimate that behavioural coaching can add around 150 bps per year by helping investors avoid common behavioural mistakes (Vanguard, Adviser’s Guide to Behavioral Coaching, 2024).

Why Is the Investor’s Biggest Enemy… the Investor Themself?

We are the most intelligent species on Earth. We invented the wheel, the steam engine, electricity, computers, the Internet, and artificial intelligence. We can send probes into space, perform surgery on the human brain, and develop technologies that only a few decades ago seemed like pure science fiction. And yet, in many everyday situations, including investing—our minds do not work as rationally as we might expect.

Even when an investor has a sound plan and strategy, the emotional part of the brain often tries to pull them away from sticking to it. For a long time, economists assumed that humans are rational beings (homo economicus), making decisions that maximize their utility or profit. Unfortunately, research (including that of Daniel Kahneman, a Nobel Prize laureate) has shown that in practice this is not the case.

This applies not only to investing but also to everyday life and business decisions. We frequently make choices that contradict our long-term goals simply to feel better in the moment, to appear consistent, or to reduce the chance of feeling disappointed.

For example, we may hold on to a stock we bought in the past even though we no longer see any growth potential in it, or we may flee the market during a bear market—even though we know it could be one of the best moments to add more capital.

You might wonder why humans are so vulnerable to traps in financial markets. The answer lies in evolution and in our history as a species. The first species classified within the genus Homo appeared on Earth several million years ago. For hundreds of thousands of years, during which our ancestors’ brains evolved, life was relatively simple and based on basic patterns: find shelter, obtain water, and secure food. Evolution therefore rewarded immediate action and risk avoidance, not long-term planning—the very skill that is crucial for successful investing.

Financial markets, however, are a very recent phenomenon from the perspective of the human brain. The first cities appeared several thousand years ago, and the earliest markets emerged around 4,500 years ago. Markets resembling the modern financial system—where stocks and bonds were traded—have existed for only about 400 years. If you imagined the entire history of humanity as a one-kilometer line, the first stock exchange would appear only about six centimeters from its end.

Our brains are brilliant at solving the kinds of problems our ancestors faced—reacting quickly to threats or recognizing simple patterns. But they are far less effective when dealing with randomness, long-term thinking, and the analysis of complex systems, such as financial markets.

Naturally, we try to see patterns and trends everywhere, even where events are largely random. This applies to coin tosses, casino games, and to some extent also to short-term stock market movements. As a result, we easily become overconfident and spend a great deal of energy trying to control things that are largely beyond our influence.

Cognitive Biases and ETFs

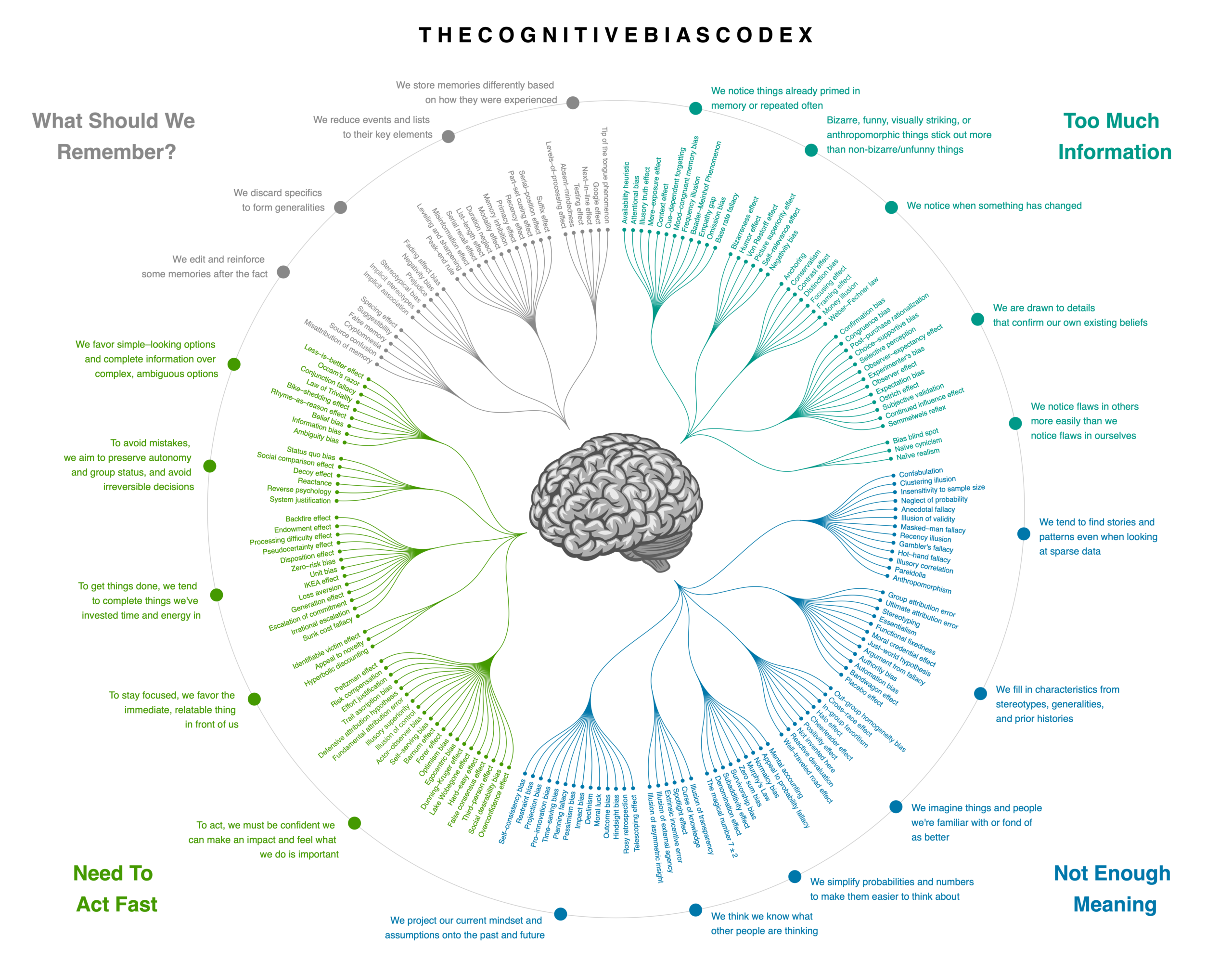

You have probably heard of some of the most common cognitive biases, such as home bias, anchoring, or loss aversion. However, these are only the beginning. Researchers have identified around 200 different cognitive biases that can influence human decision-making.

If the topic interests you, you can find a diagram along with descriptions of each bias on Wikipedia.

Figure 2. The Cognitive Bias Codex — Wikipedia’s list of cognitive biases arranged and designed as a radial diagram by John Manoogian III (jm3), based on the category model by Buster Benson; source: Wikimedia Commons (“Cognitive bias codex”).

One way to reduce the impact of these biases is to simplify the investment process. In practice, this means choosing tools that limit the temptation to constantly make decisions and “improve” the portfolio. One such tool can be ETFs tracking the broad equity market.

Thanks to their wide diversification and transparency rules, they allow investors to focus on long-term investing rather than continuously selecting individual stocks. Of course, simply buying such an instrument does not solve every problems. The key is that investors do not buy and sell under the influence of emotions, but instead consistently stick to their chosen strategy.

A similar approach has been promoted for years by Warren Buffett. Buffett has repeatedly emphasized that most investors should not attempt to pick individual stocks or predict market movements. Instead, he recommends a low-cost index fund tracking the broad market, particularly one that follows the S&P 500. As he wrote in one of his letters to shareholders, for the vast majority of investors the best solution is “regularly investing in a low-cost S&P 500 index fund”. Such a strategy does not require market forecasting or frequent decision making and reducing the number of decisions is often one of the most effective ways to avoid mistakes that lower investment returns.

Let us know if the topic of cognitive biases in investing has caught your interest and whether you would like to explore the ones that most often limit investors’ results.

If you would like to explore this topic further, we recommend the following books:

- Thinking, Fast and Slow — Daniel Kahneman

A book about the psychology of decision-making and cognitive biases, explaining how two systems of thinking operate and why people often make irrational financial decisions. - The Psychology of Money — Morgan Housel

A book on the psychology of money and investing, showing how emotions, personal history, and life experiences shape financial decisions. - Your Money and Your Brain — Jason Zweig

A publication combining finance and neuroscience, describing how the brain reacts to risk, gains, and losses during the investment process.