“Compound interest is the eighth wonder of the world”—this famous phrase, attributed to Albert Einstein, perfectly captures the power of patience and mathematics in building wealth. Many beginner investors easily grasp this mechanism in the context of bank deposits. However, many investors struggle to see this magic in the context of stock investing. After all, when investing in an ETF long-term, we simply hold the units without selling them to reinvest the profits. So, does compound interest even work here? Yes, it does. This material will explain what compound interest is, how it works for different assets, and how significant it is in long-term ETF investing.

What is compound interest and how does it work for deposits?

Compound interest is a mechanism where interest or profits earned on the capital are periodically added to its initial value, so that in subsequent periods, the interest or growth applies to the now larger amount. This is a process where profits start generating further profits, leading to exponential rather than linear wealth growth.

This mechanism is very easy to understand using the example of bank deposits. The interest received is added to the capital, and in the next period, it becomes part of the base for calculating profits.

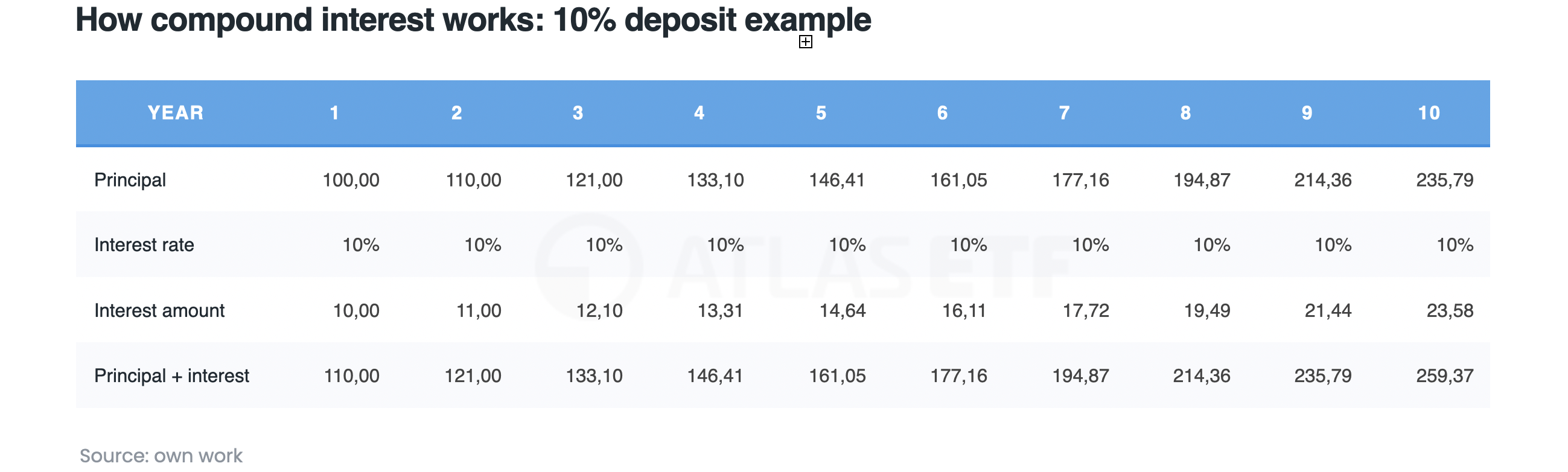

For example, if the deposit amount in the first period is 100 USD with 10% interest, after the deposit ends—with interest added—the capital is 110 USD. Assuming the same interest rate in the second period, the interest will be higher (11 USD) because the capital has grown by the previously added interest (100 + 10 = 110). This works analogously in subsequent periods.

If the interest weren’t added to the capital, after 10 periods the investor would have 200 USD on the account (100 USD + 10×10%). However, with interest capitalization, the account will show 259.37 USD. This demonstrates the “magic” of compound interest.

It works the same way for bonds and bond ETFs. Bond ETFs track total return bond indices, which assume interest reinvestment. As a result, interest in subsequent periods is higher because the capital it’s calculated from grows by the interest from previous periods.

How does compound interest work for stock ETFs?

When investing in a stock market ETF on a “buy and hold” basis, units aren’t sold to reinvest the profits. This raises the question: does compound interest even work in this case? The answer is yes.

The key to understanding it is that by investing in a stock ETF, the investor indirectly becomes a shareholder in companies. If a company pays a dividend, the investor can buy more shares with it, receiving a larger dividend next time. Of course, many companies don’t pay dividends but reinvest profits—which positively impacts the share price on the exchange, creating a similar effect to a dividend payout. This shows that the compound interest mechanism works here just like with a deposit.

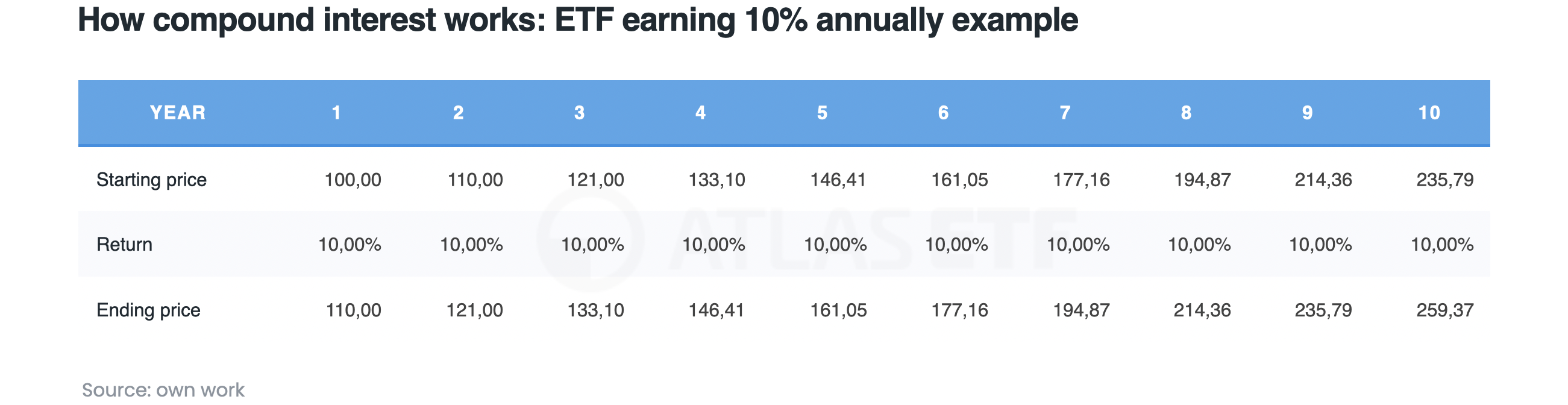

It’s worth illustrating with an example. Suppose an ETF earns 10% in the first year and another 10% in the second. The return after 2 years isn’t 20%, but 21%.

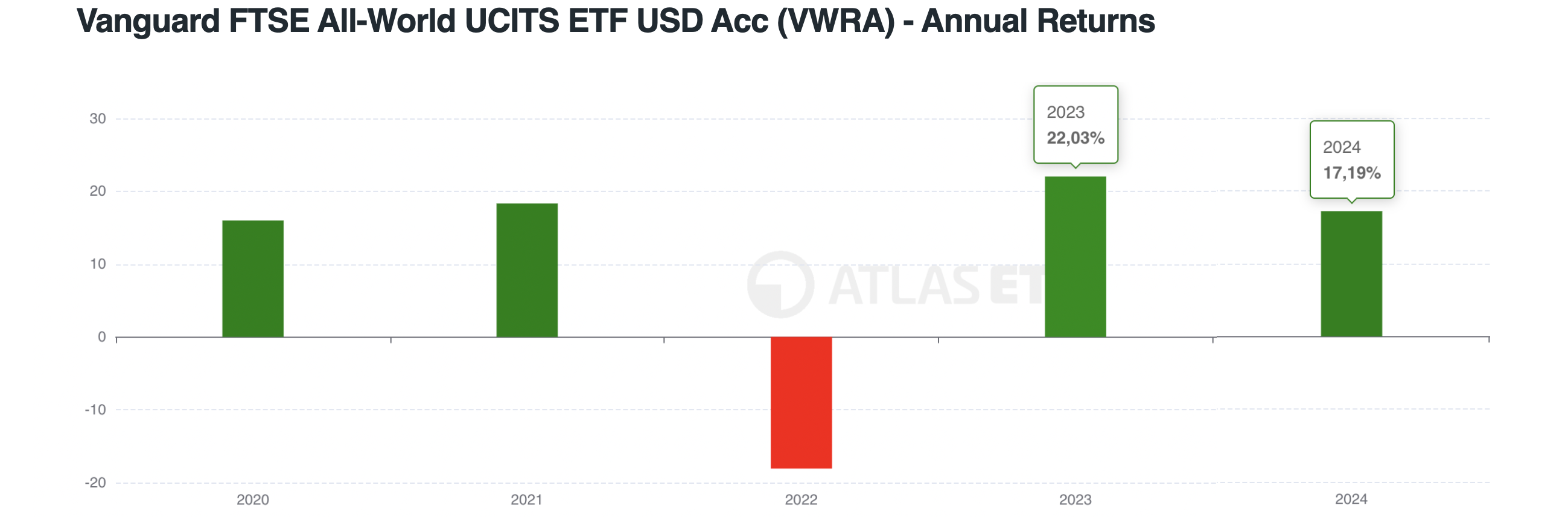

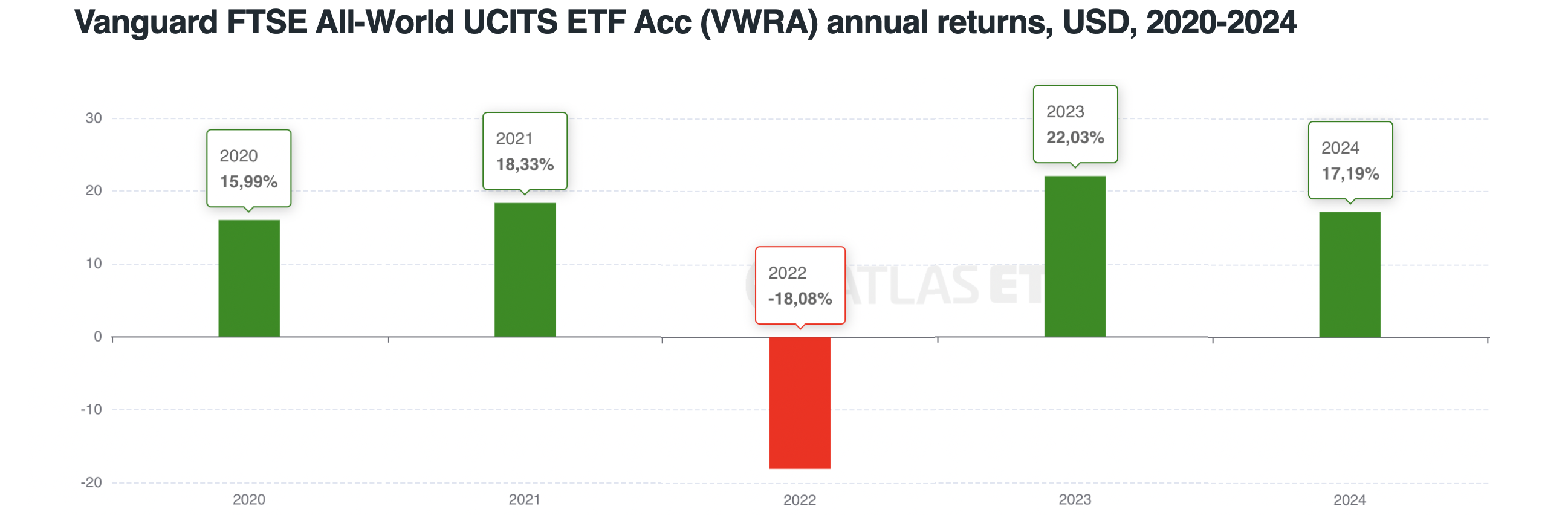

A real ETF example shows this even better. The Vanguard FTSE All World UCITS ETF Acc achieved a return of 22.03% in 2023 and 17.19% in 2024 (in USD). A simple sum of these returns would be 39.22%. However, that’s not the actual result the fund achieved over 2 years.

The real result was higher: from January 1, 2023, to December 31, 2024, the price rose by 43%—almost 4 percentage points more.

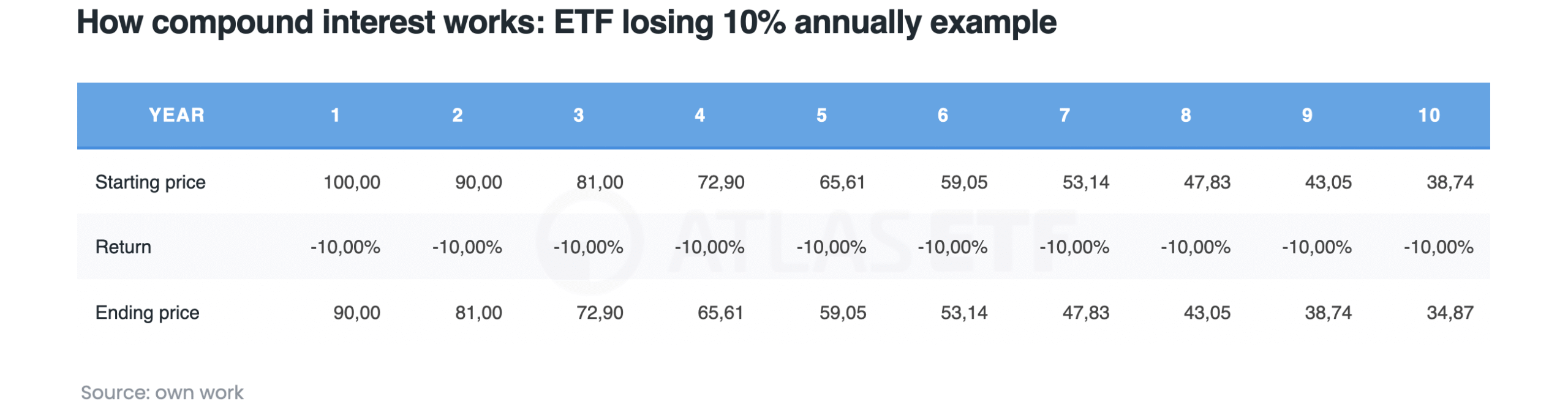

Of course, ETFs can not only rise but also fall—compound interest then works “downward.” If an ETF loses 10% each year, the loss after two years isn’t -20%, but -19% (starting price in year 1 was 100, ending price in year 2 is 81).

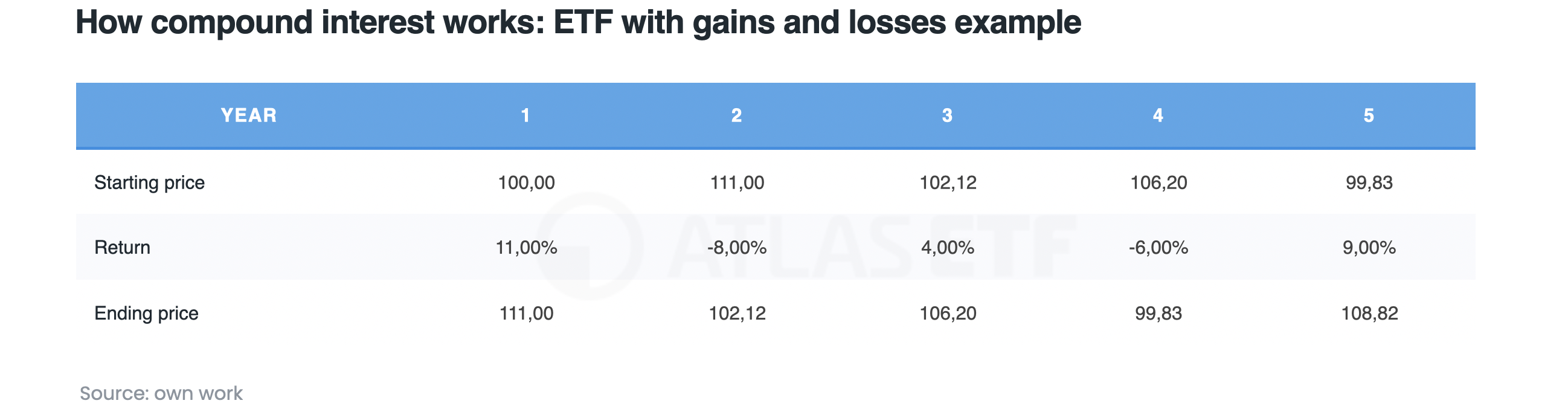

In practice, ETFs have both profitable and loss-making years, which further highlights the error of simply summing returns. Take a hypothetical fund with returns: +11%, -8%, +4%, -6%, +9%. The simple sum is 10%, but the actual return is 8.82% (ending price after 5 years is 108.82).

This is even clearer with the aforementioned Vanguard FTSE All World UCITS ETF Acc (VWRA). In 2020, 2021, 2023, and 2024, it posted gains (15.99%, 18.33%, 22.03%, 17.19%), and in 2022 a loss of -18.08%. A simple sum of the annual returns would be 55.46%, but that wouldn’t be the actual return achieved in that period.

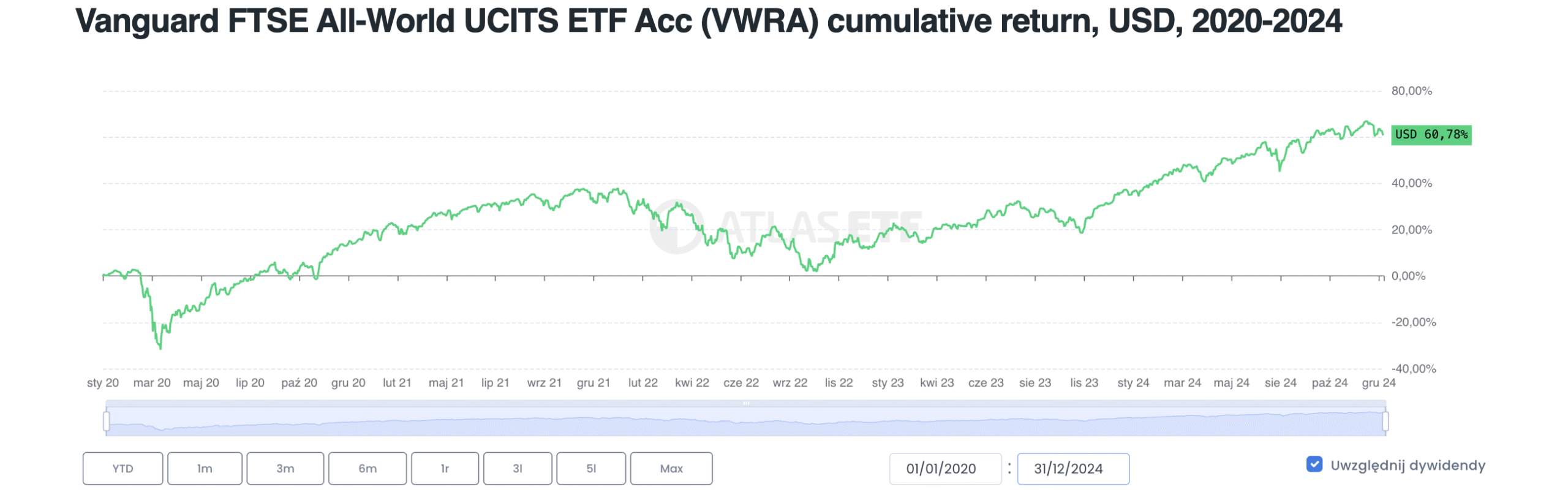

The actual return over this period was 60.78%—over 5 percentage points more.

Do distributing ETFs prevent compound interest?

So far, we’ve assumed dividends get reinvested – in the examples, we used the Vanguard FTSE All World UCITS ETF Acc (VWRA), the accumulating version of the fund. But does compound interest work at all without dividend reinvestment? Yes, it does, but not as strongly.

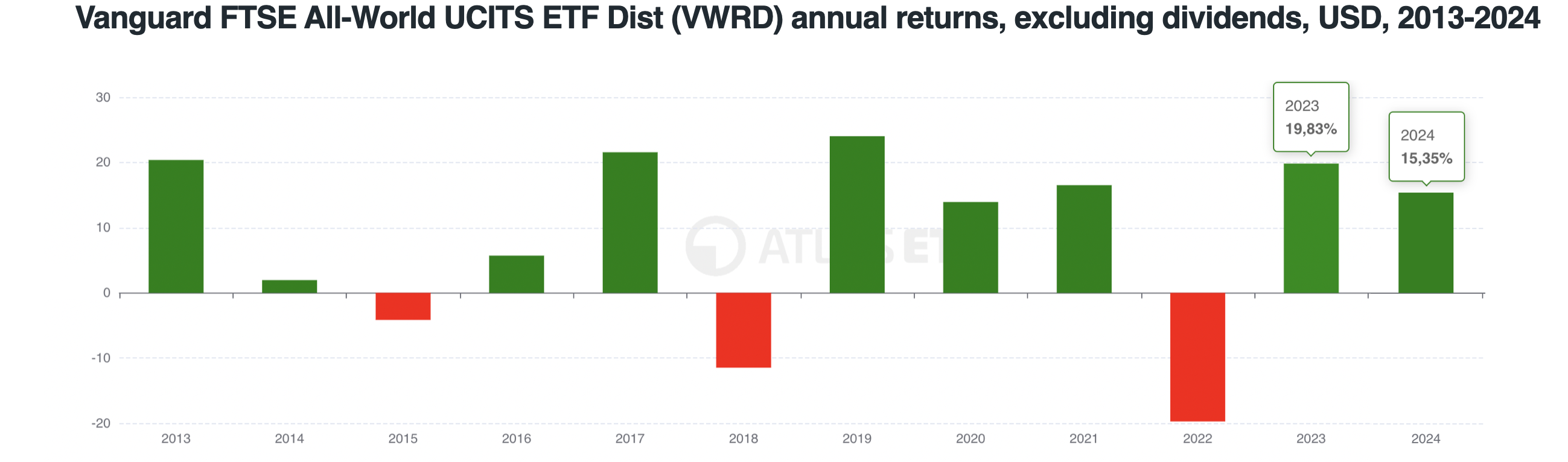

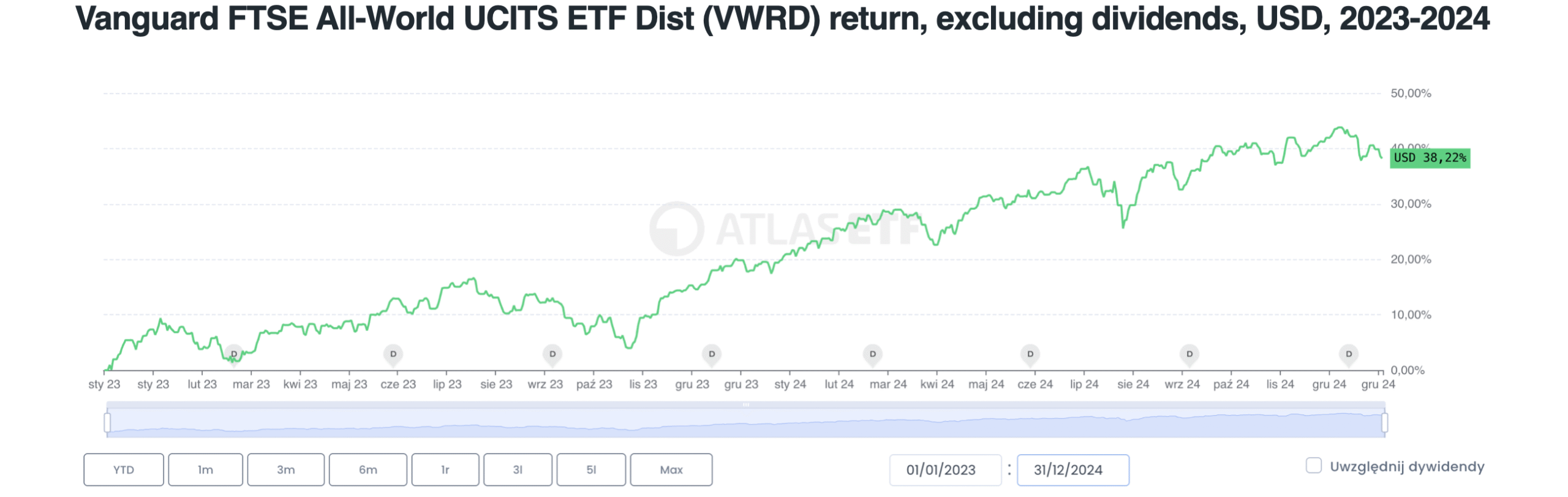

This time, let’s take the distributing version: Vanguard FTSE All World UCITS ETF Dist (VWRD). In 2023 and 2024, the fund achieved returns of 19.83% and 15.35%. These are results excluding dividends, reflecting the situation where the investor receives the dividend but doesn’t reinvest it—instead spends it. A simple sum for these two years would be 35.18%, but that wouldn’t be the actual gain.

The real unit price growth was 38.22%—over 3 percentage points more.

In the same period, the accumulating (Acc) version delivered a result 4 percentage points higher, not 3. This leads to the conclusion: while compound interest works even without dividend reinvestment, dividends significantly enhance this effect. Over the long term, the differences can be colossal.

Does compound interest work for assets like gold and cryptocurrencies too?

When investing in company stocks (e.g., via ETFs), compound interest works regardless of whether the company reinvests profits or pays them out as dividends (which the investor can use to buy more shares). But does compound interest work for “non-working” assets like precious metals (e.g., gold) or cryptocurrencies (e.g., bitcoin)?

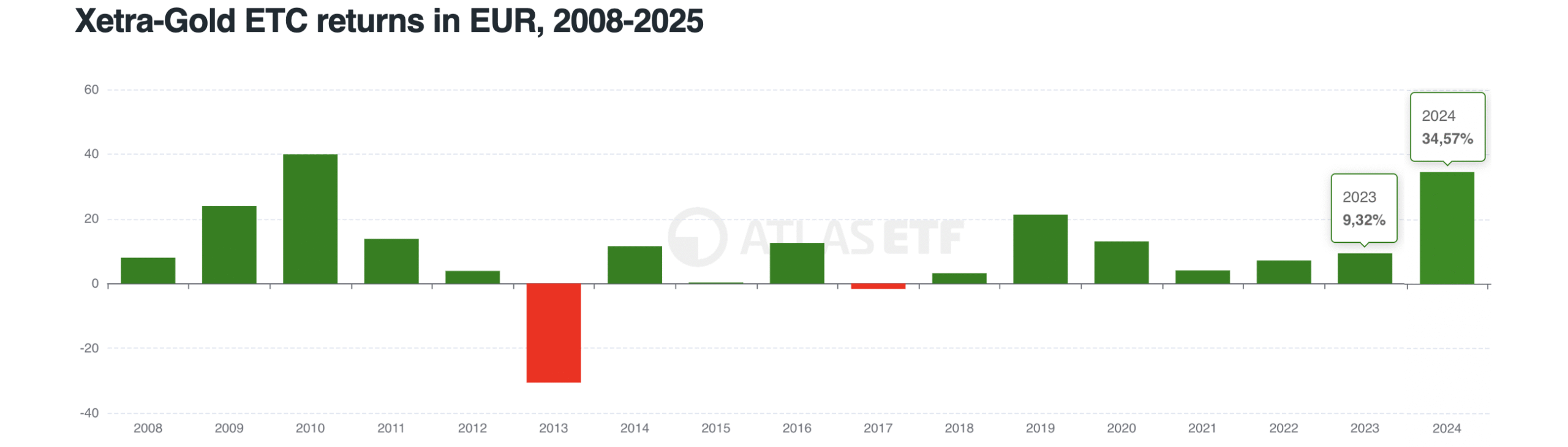

Yes—compound interest works here through reinvesting gains from price appreciation, even if it’s not immediately obvious. Example: Xetra-Gold ETC in 2023–2024 (in EUR) achieved returns of 9.32% and 34.57%. A simple sum would give 43.89%.

Meanwhile, an investor who bought Xetra-Gold at the start of 2023 could enjoy a 47.11% return by the end of 2024—over 3 percentage points higher.

For other non-working assets like cryptocurrencies (e.g., bitcoin), it works similarly. To verify this, visit atlasETF.pl, open the page for any instrument, go to the Chart tab, check returns for selected periods (e.g., annual), and compare them to the total return for the entire period (which you can read from the chart).

How important is compound interest over the long term?

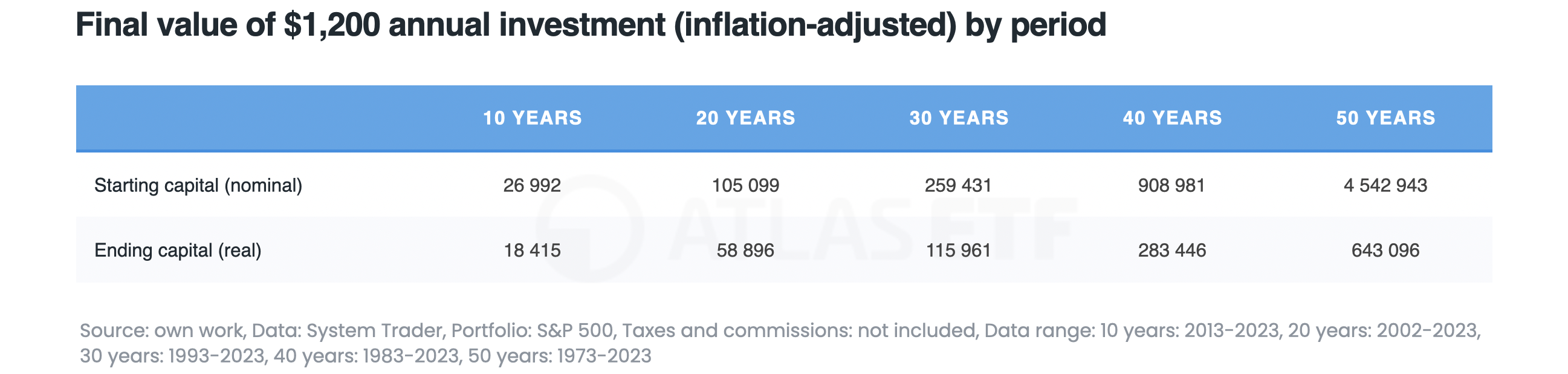

The magic of compound interest over the long term can work wonders. To see its true power, let’s analyze an investment in US stocks (S&P 500) using real historical data, adjusted for US inflation. In the first year, $1,200 was invested annually ($100 monthly), and in subsequent years, the amount was increased by inflation.

The final nominal amounts are impressive, but they ignore inflation, so it’s better to look at real amounts that account for it. After 10 years, $18,415 was accumulated (in real terms). After 30 years (3 times longer)—$115,961, or over 6 times more. After 50 years (5 times longer)—$643,096, or nearly 35 times more.

As you can see, capital growth isn’t linear but exponential. This is exactly what shows the magic of compound interest: the longer the period, the more powerful the effect. It also proves that investing seemingly small amounts over a long time can build substantial capital.

Summary

The “eighth wonder of the world”—compound interest—works not just on deposits, but also in ETFs, gold, and cryptocurrencies, driving exponential capital growth. Simply adding up annual returns is misleading—actual results are higher thanks to profit reinvestment (or price appreciation). Even distributing ETFs benefit from this mechanism, though less than accumulating ones. Compound interest shows its true power over the long term: even seemingly small investments can build impressive capital.