ETFs (Exchange Traded Funds) are modern and flexible investment instruments that provide easy access to various asset classes at low cost and with high liquidity. Their popularity stems from their simple structure and wide availability for investors worldwide. However, to effectively utilize the opportunities offered by ETFs, it is worthwhile to understand their key features, learn how to read their names, and grasp the differences between European and American funds. Below are the key elements of ETF characteristics.

Fund Domicile (ETF Registration Location)

The domicile is the country where the ETF has been formally established and where it is subject to local legal regulations and financial supervision. This is one of the key parameters to check before investing, as it affects the safety of funds, investor protection, taxation, and the fund’s availability in various markets.

Why is the domicile important?

- Investor protection, regulations, and oversight: Funds registered in the European Union (e.g., in Ireland or Luxembourg) must meet stringent UCITS (Undertakings for Collective Investment in Transferable Securities) directive requirements. UCITS ensures a high level of transparency, asset safety, and limits risk (e.g., by imposing concentration limits and requiring assets to be held by an independent custodian). Funds registered in the USA are supervised by the SEC (Securities and Exchange Commission) and must comply with American legal standards, which differ from European ones,

- Taxes: The domicile affects how dividends and capital gains are taxed,

- Availability: European ETFs (UCITS) are widely available to investors from EU countries, while American ETFs may be inaccessible to Europeans due to PRIIP regulations (Packaged Retail and Insurance-based Investment Products – an EU regulation aimed at increasing retail investor protection by introducing uniform and transparent rules for investment products like mutual funds, ETFs, structured products, or insurance-based investment products).

Fund Name

ETF names are constructed according to specific rules, allowing investors to glean key product information at first glance. Names often include elements such as the provider, index type, dividend policy, or base currency. Importantly, there are clear differences in naming conventions between American and European ETFs.

European-registered fund names are usually more detailed, while American ETFs have shorter, simplified names. The ability to decipher these names allows investors to quickly identify the type of fund, the market or index it tracks, and whether it meets European regulatory standards. Knowing how to read ETF names enables efficient product comparison during initial selection.

Currently, ETFs available in the European market, in line with the aforementioned PRIIP regulations, are required to publish a KID (Key Information Document). The KID is a basic information document containing key data about the ETF, such as product characteristics, risk level, costs, return scenarios, and recommended investment horizon. This document is intended to allow retail investors to easily compare different products and better understand the potential benefits and risks of investing in an ETF.

Previously, UCITS funds used the KIID (Key Investor Information Document), but under PRIIPs regulations, the KID has replaced the KIID for most ETFs available to retail investors in Europe. The presence of both documents for a single ETF results from the need to meet different regulatory requirements and ensure information transparency for all potential investors during the transition period. In the coming years, the KID will fully replace the KIID for funds available to retail clients in the EU.

After searching for a selected ETF, you can find a complete set of documents for the fund on etfatlas.com.

⚠️ Note

To obtain information about a specific fund, it is worth using an ETF search engine. To find a given fund, enter its ISIN, ticker, or name (or at least part of it) in the search field.

How to Read an ETF Fund Name?

An ETF fund name is not only a marketing element but also a source of key information about the product’s characteristics. Proper interpretation of the name allows for quick determination of the fund’s assets, manager, dividend policy, and the currency in which its units are valued.

Key elements of an ETF name:

- Provider: Indicates the company managing the fund, e.g., Vanguard, Invesco, SPDR. A reputable provider often means greater safety and lower management costs,

- Index/strategy: Indicates which index the fund tracks, e.g., S&P 500, MSCI World, FTSE All-World. Knowing the index allows you to determine the assets in the ETF’s portfolio,

- UCITS: Indicates compliance with the EU UCITS directive, typical for European ETFs. American funds lack this designation,

- ETF: Abbreviation indicating the type of instrument,

- Currency: Specifies the fund’s base currency in which units are valued (e.g., USD, EUR), usually given in parentheses,

- Dividend policy: Indicates whether dividends are reinvested (Accumulating, Acc) or paid out to investors (Distributing, Dist). American funds lack this designation.

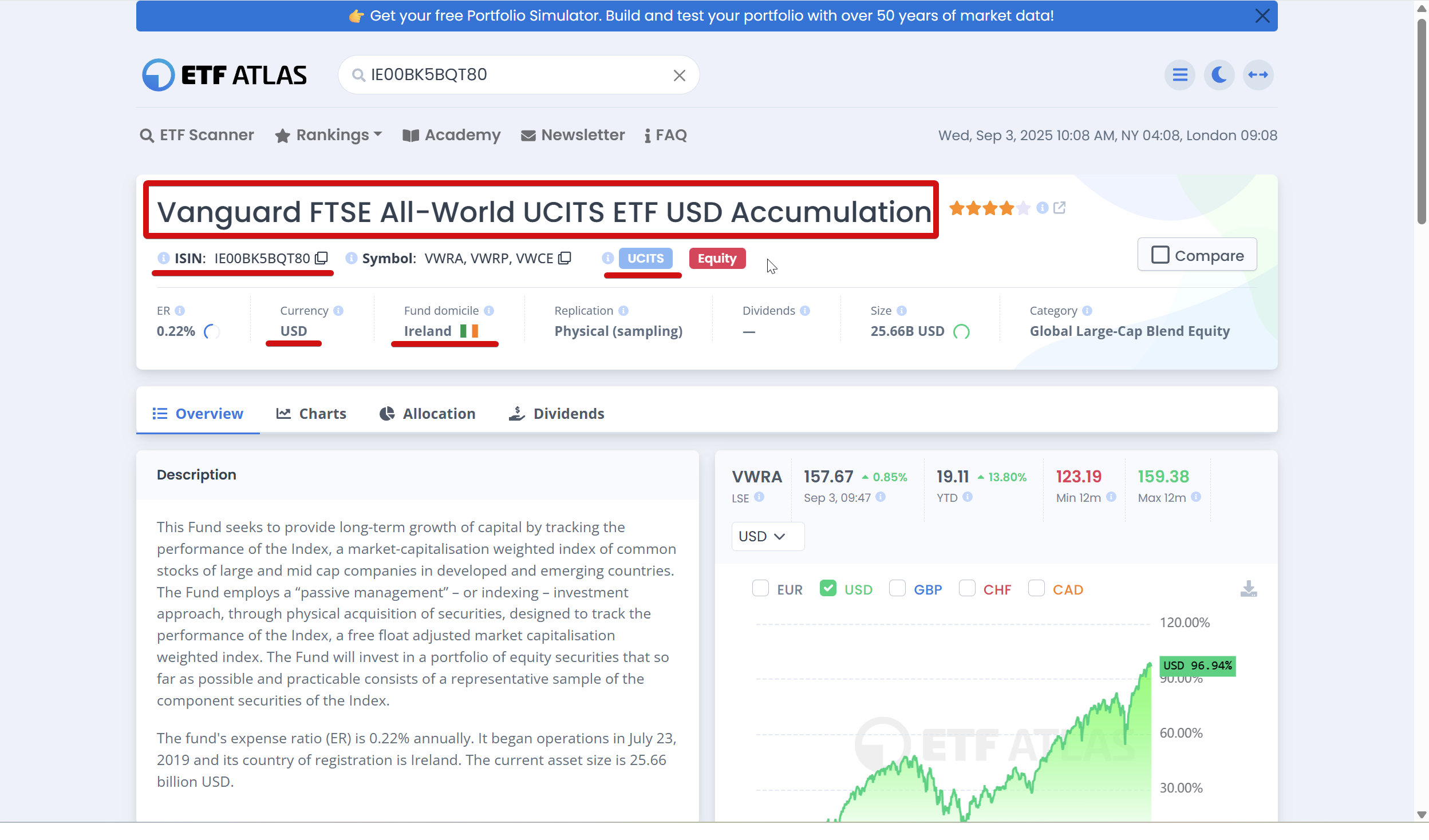

Example (European ETF): Vanguard FTSE All-World UCITS ETF (USD) Accumulation

- Vanguard – provider

- FTSE All-World – index

- UCITS – EU regulation compliance

- ETF – instrument type

- (USD) – base currency

- Accumulation – dividend policy (dividends reinvested)

Example (American ETF): Vanguard S&P 500 ETF

- Vanguard – provider

- S&P 500 – index

- ETF – instrument type

Lack of information on dividend policy, currency, or UCITS suggests it is likely an American ETF.

Sometimes, instead of “ETF“, the fund name includes “Trust” or “ETF Trust” e.g., SPDR S&P 500 ETF Trust. This refers only to the fund’s legal structure, not its investment strategy.

Properly reading a fund’s name enables quick comparison of different ETFs and preliminary matching of products to your investment needs before analyzing detailed documents.

ISIN Code – Unique Fund Identifier

ISIN (International Securities Identification Number) is a 12-character international unique code used to identify each financial instrument, including ETFs. The ISIN is used globally and allows precise differentiation of investment products regardless of listing market or local symbols.

In practice, the ISIN helps eliminate errors, especially when the same fund is listed on different exchanges under various tickers or in different currencies. This assures investors and financial institutions that they are transacting the correct instrument.

The first two letters of the ISIN code indicate the fund’s country of registration, further aiding product identification (e.g., IE – Ireland, LU – Luxembourg, US – United States).

Examples:

- Vanguard FTSE All-World UCITS ETF (USD) Accumulating – ISIN: IE00BK5BQT80

- Vanguard S&P 500 ETF – ISIN: US9229083632

Using the ISIN allows for unambiguous identification of an ETF, regardless of listing location or broker.

Strategy (Index)

An ETF’s strategy involves tracking a specific stock index or other benchmark. An index is a compilation of selected assets, such as stocks, bonds, or commodities, designed to reflect the performance of a particular market, sector, or economy segment. The choice of index determines the ETF’s portfolio composition and exposure to specific asset classes, geographic regions, or industries.

The most common ETF strategy is passive, aiming to closely replicate the performance of the chosen index without active portfolio management. This provides investors with broad diversification and transparency, while keeping management costs low.

Examples:

- iShares Core MSCI World UCITS ETF – tracks the MSCI World index, providing exposure to developed market stocks,

- SPDR S&P 500 ETF Trust – tracks the S&P 500 index, focusing on the largest US companies.

The choice of strategy, i.e., base index, is crucial for determining risk profile, potential returns, and the geographic and sectoral allocation of the ETF portfolio.

It is also worth noting that actively managed ETFs are increasingly appearing in the market. Unlike traditional passive ETFs, these products do not have to strictly track any specific index. Managers have more freedom in portfolio selection, aiming for above-average returns. However, even for actively managed ETFs, a benchmark index is often indicated for performance comparison.

Fund Currency (Base Currency)

The fund’s currency determines the currency in which the ETF units are valued. This is the so-called fund base currency. This information is usually included in the ETF’s name, especially for funds listed in Europe, e.g., (USD), (EUR), (GBP). It serves a statistical function – the fund’s performance is presented in this currency.

It is also worth noting that the same ETF can be listed on different exchanges in different currencies. This means that investors can choose the version of the ETF that best suits their currency preferences and the availability offered by a given broker. Regardless of the selected exchange or currency, all these listings refer to the same fund (with the same ISIN code), and price differences result from exchange rate conversions and local market conditions. This makes it possible to reduce currency conversion costs and provides easier access to the ETF within the investor’s chosen trading platform.

It should be emphasized that neither the fund’s currency nor the trading currency has an impact on the currency risk. Its source is the currency of the assets in which the fund invests. For example, if a fund invests half of its assets in U.S. stocks (in USD) and the other half in German stocks (in EUR), while the investor’s currency is the British pound (GBP), then the investor is exposed to USD/GBP currency risk (50%) and EUR/GBP currency risk (50%).

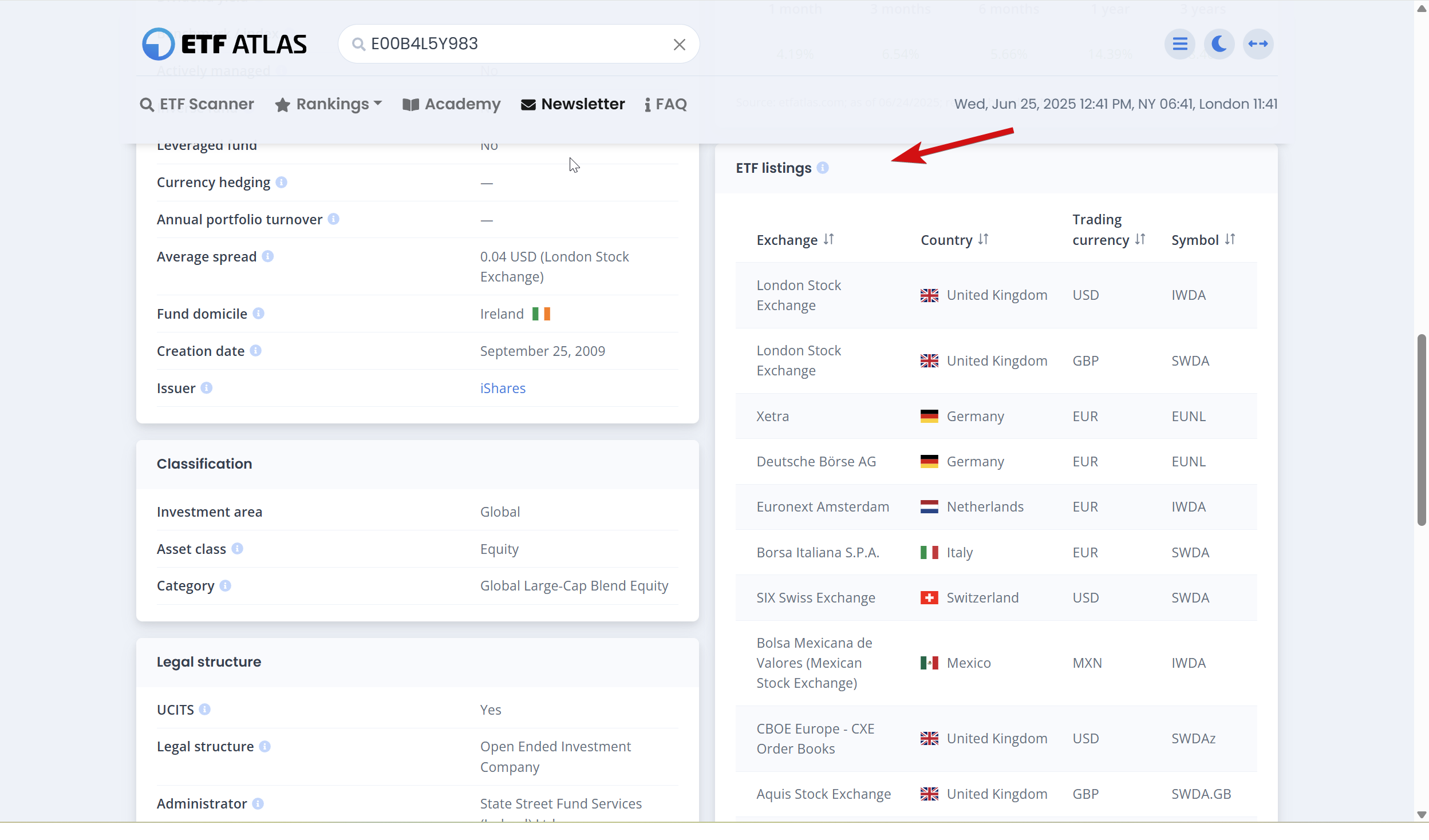

On our website, in the fund quotation section, detailed information about each ETF is available, including the list of exchanges, trading currencies, and assigned tickers, allowing for quick verification of where and under what symbol the fund is listed. Below is an example of the ETF iShares Core MSCI World UCITS ETF (ISIN: IE00B4L5Y983), which is listed on different exchanges in various currencies.

Currency Hedging

Currency hedging is a strategy that protects investments from exchange rate fluctuations. Currency risk arises when an ETF invests in assets denominated in a foreign currency, while the investor settles in another currency. Exchange rate changes can both increase and decrease the investment’s value after conversion to the investor’s domestic currency. Currency appreciation can positively impact returns, while depreciation can have a negative effect.

To eliminate this factor, currency hedging is used, i.e., protection against exchange rate fluctuations. In practice, ETFs use derivatives such as futures, currency options, or swaps for this purpose. As a result, exchange rate changes do not affect the final investment outcome – the investor receives index performance regardless of currency fluctuations.

ETFs with currency hedging are often marked in their names as “hedged” to a specific currency, e.g., EUR-Hedged, USD-Hedged, GBP-Hedged. Currency hedging is most commonly used in bond funds and ETFs on precious metals and commodities, where exchange rate volatility can significantly impact investment results. In Europe, about 20% of ETFs use currency hedging, with an even higher share among bond funds.

Example:

A popular currency-hedged ETF is iShares Core Global Aggregate Bond UCITS ETF EUR Hedged – Acc. This fund invests globally in bonds and hedges currency risk to the euro, so exchange rate changes do not affect the investment outcome in euros.

Similar solutions are used in other funds, e.g., Xtrackers II Global Government Bond UCITS ETF 1C – EUR Hedged, or iShares Global Corp Bond EUR Hedged UCITS ETF – Dist, which hedge investment results to the euro.

Such ETFs are especially popular among investors seeking to limit currency risk and gain foreign market exposure without the impact of currency fluctuations. Currency hedging allows investors to achieve results similar to those of the base index in the hedged currency.

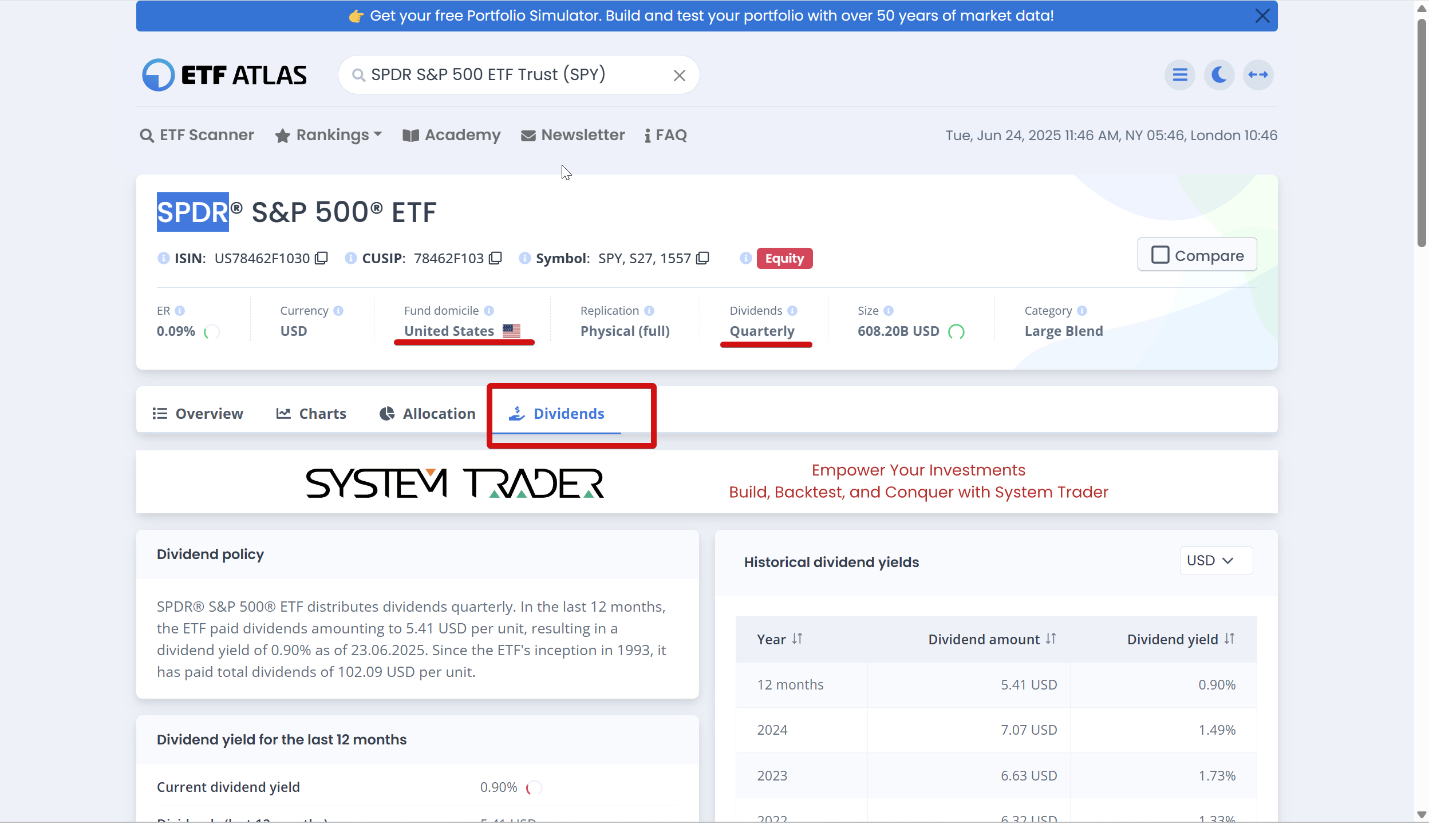

Dividend Policy

The dividend policy in ETFs determines how the fund handles dividends received from companies in its portfolio. There are two basic models:

- Distributing dividends to investors (distributing),

- Accumulating dividends within the fund (accumulating).

Both types are available in the European market. Dividend-distributing ETFs, usually marked as “Distributing” or “Dist“, pay out received funds directly to the investor’s account, most often quarterly, semi-annually, or annually. An example is SPDR S&P Euro Dividend Aristocrats UCITS ETF (Dist), which regularly pays dividends to its participants.

Accumulating funds, marked as “Accumulating” or “Acc“, reinvest dividends within the fund, increasing the value of participation units. An example is Amundi MSCI Europe High Dividend Factor UCITS ETF EUR (C), where dividends are automatically reinvested.

In the US market, the cash dividend payout model dominates. Most US ETFs pay dividends to investors, usually quarterly. An example is SPDR S&P 500 ETF Trust (SPY), which regularly pays dividends. Accumulating funds are rare in the US, and dividend reinvestment is usually done through automatic purchase programs (DRIP – Dividend Reinvestment Plan), but formally each dividend is paid out and taxed.

Information about the dividend policy is usually found in the ETF’s name or documentation. The dividend policy is an important feature of an ETF and should be matched to individual needs and investment strategy.

Index Replication Methods

The replication method determines how the ETF tracks the performance of its chosen benchmark index. The chosen method affects the accuracy of index tracking, risk level, costs, and fund transparency.

Types of replication:

- Full physical replication

- Partial physical/representative sampling

- Synthetic

- Hybrid

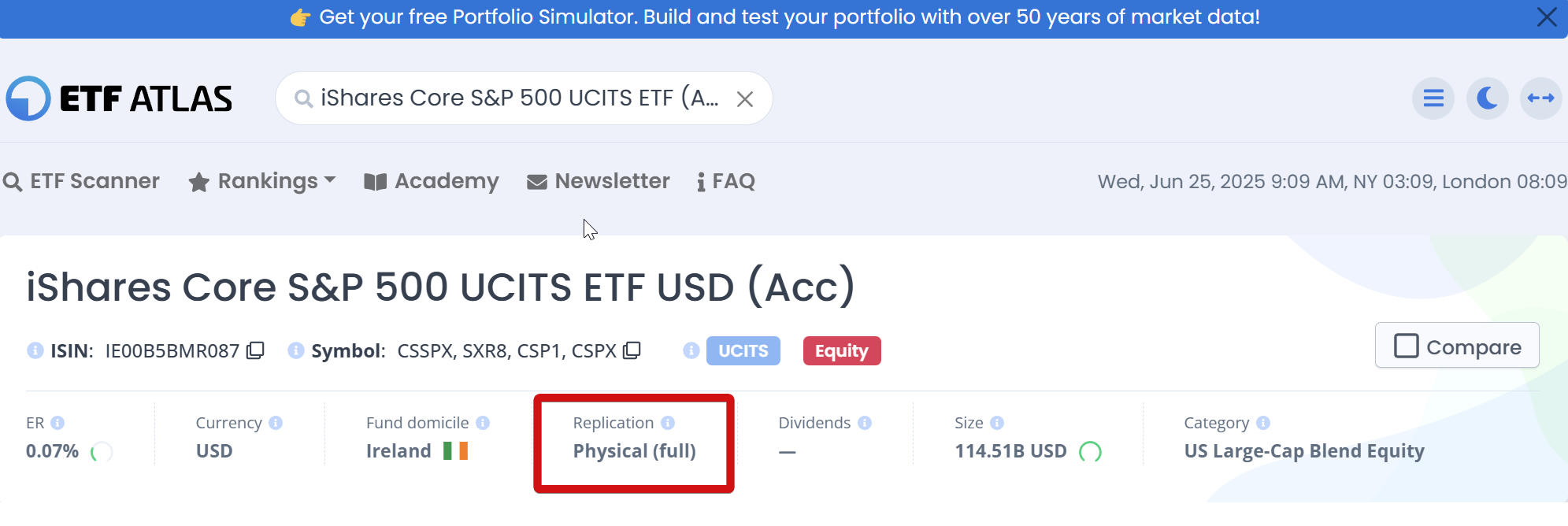

Full Physical Replication

With full physical replication, the fund buys all the components of the benchmark index in proportions matching their index weights. This means the ETF portfolio is almost identical to the index portfolio, ensuring high transparency and minimizing counterparty risk.

Example: iShares Core S&P 500 UCITS ETF (Acc) tracks the S&P 500 index by purchasing shares of all 500 companies in the index.

Partial Physical Replication

Also known as representative sampling. The fund buys only a selected portion of index assets most representative of its structure and behavior. This method is used for very broad or hard-to-access indices, where buying all components would be inefficient or costly.

Example: iShares Core MSCI Europe UCITS ETF EUR (Acc), which covers nearly 400 companies from 15 developed European countries. Instead of buying all index stocks, the fund uses “optimized sampling,” selecting a representative sample to efficiently track the index at lower cost and greater flexibility.

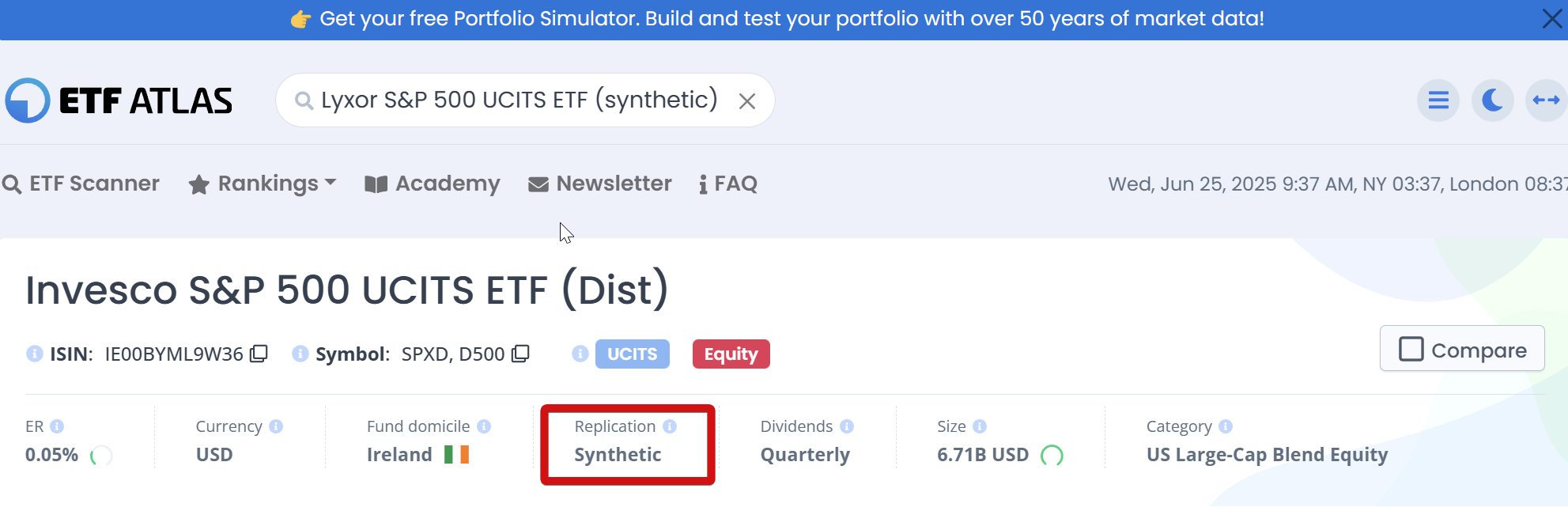

Synthetic Replication

Synthetic replication involves tracking index performance using derivatives, usually swaps. The fund does not physically hold index assets but enters into agreements with financial institutions that pay the fund returns matching the index. This method enables tracking of hard-to-access indices or illiquid markets but involves counterparty risk. It is also used for tax optimization, e.g., to avoid US withholding tax when investing in American stocks. Such ETFs may achieve slightly better results than those using physical replication (where withholding tax applies).

Example: Invesco S&P 500 UCITS ETF (Dist) tracks the S&P 500 index using swaps, not direct stock purchases.

Hybrid Replication

Hybrid ETFs combine elements of both physical and synthetic replication in one fund. Part of the portfolio is replicated through direct purchase of actual index securities (physical), and the rest through derivatives, usually swaps (synthetic).

Hybrid ETFs make up a small percentage of the ETF market. They are most common in global funds, broad equity or bond indices, where different markets require different replication approaches. Most ETFs use physical or synthetic replication, while hybrid solutions are chosen where they offer significant cost, tax, or operational benefits.

Example: Scalable MSCI AC World Xtrackers UCITS ETF 1C. This fund uses hybrid replication, combining physical replication (direct stock purchases from some markets) and synthetic replication (e.g., swaps for less accessible or less tax-efficient markets like the USA or China). This allows the ETF to efficiently track a broad global index while maintaining low costs and high flexibility.

On our website etfatlas.com, this fund is listed as synthetic, as the data comes from the Morningstar database and is presented according to their classification.

In summary, the replication method affects the ETF’s risk profile, costs, and transparency. Information on the chosen method is found in the fund’s documentation and should be considered when making investment decisions.

Listing Markets

As their name suggests, ETFs (Exchange Traded Funds) are listed on stock exchanges worldwide. The largest number of ETFs can be found in the United States and Europe, but access is also available in markets such as Asia and Latin America.

United States

In the USA, ETFs are mainly concentrated on two exchanges:

- NYSE Arca (New York) – the world’s largest ETF market

- NASDAQ – also lists hundreds of ETFs

As of September 2025, over 4,500 ETFs are listed in the US market, making it the most developed and liquid ETF market globally.

Europe

In Europe, ETF trading is spread across many exchanges. The largest and most important include

- Xetra (Frankfurt)

- Gettex (Munich)

- London Stock Exchange (London)

- SIX Swiss Exchange (Zurich)

- Borsa Italiana (Milan)

- Börse Stuttgart (Stuttgart)

- Euronext (covering Paris, Amsterdam, Brussels, Lisbon, and Dublin exchanges)

According to the latest data, over 5,100 ETFs are listed in the European market, largely due to a fragmented market (many currencies, countries, and exchanges).

Listing markets are an important ETF characteristic, affecting liquidity, availability, and the ability to buy in the chosen currency. The choice of listing market depends on investor preferences, broker availability, and planned investment currency.

ETF Tickers

A ticker is a unique, short letter code assigned to each ETF on a specific exchange. It allows quick searching and identification of the fund in trading systems and with brokers.

Differences in tickers: USA vs Europe

In the USA, ETFs are almost always listed on a single exchange and have one, fixed ticker. If, however, the same ETF were listed on more than one exchange (which is rare), the same ticker would be used on each – this is standard for dual-listed stocks. In practice, dual ETF listings in the USA are almost unheard of, so investors do not need to worry about different tickers for the same fund, as is common in Europe, where the same ETF may have different tickers on different exchanges.

- USA: ETF tickers are usually short, 3- or 4-letter codes (e.g., SPY, VOO, QQQ). Each ETF has one ticker per exchange (e.g., NYSE Arca, NASDAQ).

Examples: SPDR S&P 500 ETF Trust is listed on NYSE Arca as SPY, and Invesco QQQ Trust on NASDAQ as QQQ.

- Europe: The same ETF can be listed on several exchanges under different tickers and in different currencies. European tickers are usually 4-letter codes (e.g., VWCE, EUNL, SWDA) and differ depending on the exchange and trading currency.

Examples:

iShares Core MSCI World UCITS ETF (ISIN: IE00B4L5Y983):

- Xetra (Germany, EUR): EUNL

- Euronext Amsterdam (Netherlands, EUR): IWDA

- London Stock Exchange (UK, GBP): SWDA

- Borsa Italiana (Italy, EUR): SWDA

Vanguard FTSE All-World (Acc) (IE00BK5BQT80):

- Xetra (Germany, EUR): VWCE

- London Stock Exchange (UK, USD): VWRA

iShares Physical Gold ETC (IE00B4ND3602) on the London exchange is listed in different currencies under the tickers:

- EGLN — EUR

- IGLN — USD

- SGLN — GBX (pence)

A notable example where an investor can easily make a costly mistake is the ticker EUNA, which can mean completely different funds on different European exchanges:

- Euronext Amsterdam: iShares STOXX Europe 50 UCITS ETF EUR (Dist)

- Xetra or Gettex: iShares Core Global Aggregate Bond UCITS ETF EUR Hedged (Acc)

Therefore, always check not only the ticker but, above all, the fund’s ISIN to avoid mistakes when purchasing.

⚠️ Note

In the USA, ETF tickers are so popular that investors often use them in everyday conversation, and some, like SPY or QQQ, have become icons of the financial market.

Assets Under Management (AUM)

Assets Under Management (Assets Under Management, AUM) is the total value of capital managed by the ETF on behalf of its investors. It is the sum of the market value of all assets held by the fund, such as stocks, bonds, cash, or derivatives. AUM is one of the key metrics when assessing an ETF.

Significance of AUM

A high asset value indicates popularity and investor trust in a given ETF. Funds with large assets are usually more liquid, making trading easier and reducing bid-ask spreads. Large AUM also allows for economies of scale, potentially resulting in lower management costs for investors.

Conversely, ETFs with low assets may be less available at brokers and more prone to liquidation or transformation due to unprofitability. It is generally assumed that an asset level of around EUR 100 million ensures fund stability and profitability. Funds below this value may be closed, and funds returned to investors, necessitating a new product selection and possible tax consequences.

How is AUM calculated?

AUM is calculated as the sum of the market value of all assets in the ETF portfolio. In practice, this means multiplying the number of securities held by their current market prices, summing these values, and possibly subtracting fund liabilities.

Examples:

- Vanguard S&P 500 ETF (VOO) – one of the world’s largest ETFs, with assets exceeding USD 700 billion (September 2025),

- iShares Core MSCI World UCITS ETF – assets over USD 100 billion.

- ETFs with low assets – funds with assets below EUR 100 million are less liquid and more prone to liquidation.

AUM is an important criterion when choosing an ETF, as it affects liquidity, availability, stability, and investment costs. Large AUM usually means greater certainty, lower costs, and easier trading, while small funds may involve additional risks for the investor.

Management Costs

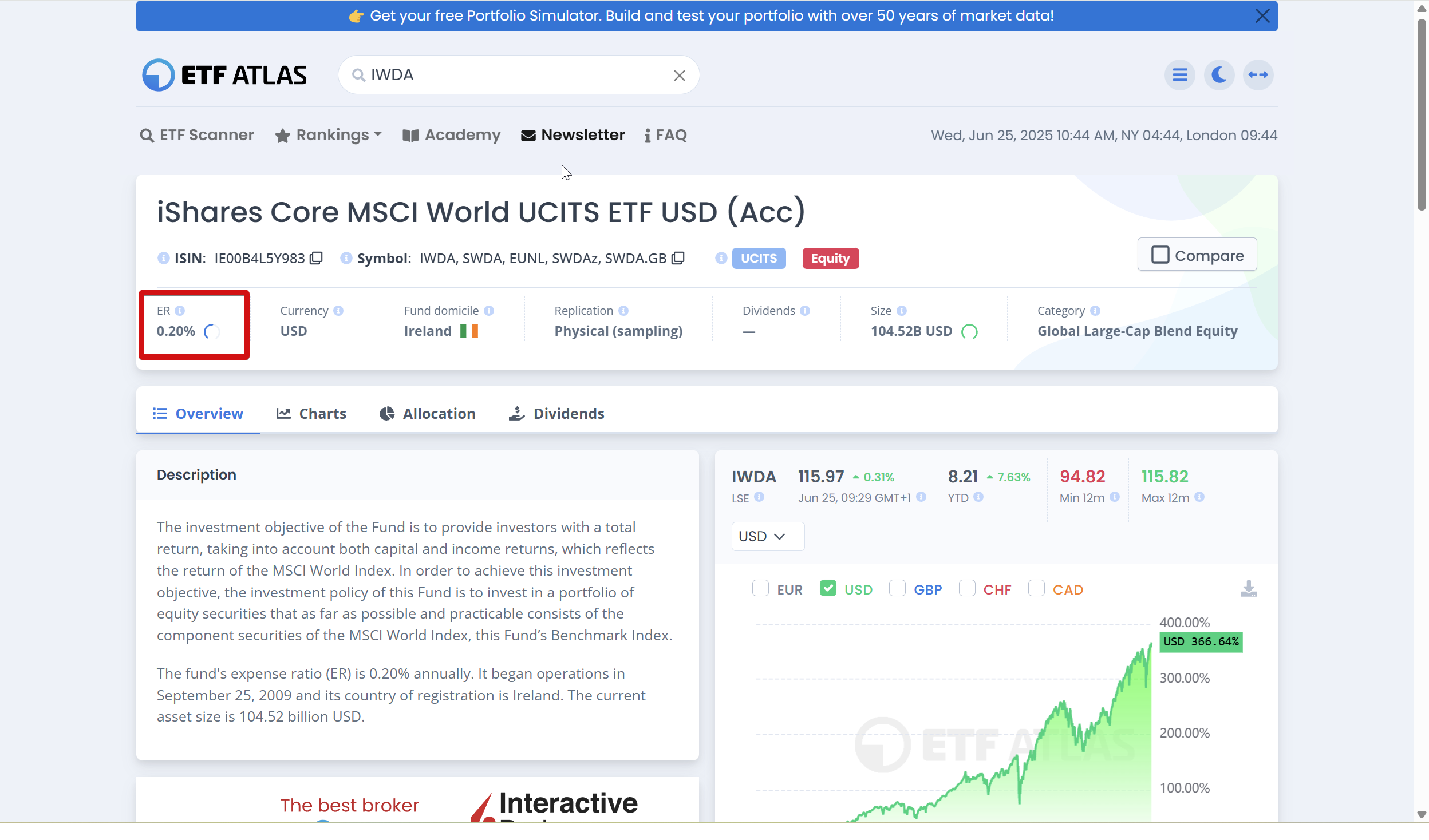

ETF management costs, most often referred to (though this includes more than just management fees) as TER (Total Expense Ratio) or ER (Expense Ratio), are one of the most important parameters when choosing a fund. TER includes all fixed fees charged by the fund manager, including management, administration, and operational costs, expressed as a percentage of assets annually. Even small differences in TER can significantly affect long-term investment results, as these fees are automatically deducted from fund assets and reduce returns.

ETF costs in Europe

In the European market, the average TER for ETFs is about 0.33% per year, with the cheapest index funds (“plain vanilla”) having costs as low as 0.05–0.20%. ETFs with more complex strategies, such as those on commodities, bonds, or emerging markets, have higher costs – often in the 0.4–0.5% range or more.

Examples:

Popular ETF iShares Core MSCI World UCITS ETF (IWDA) has a TER of 0.20%, and Vanguard FTSE All-World UCITS ETF (VWCE) – 0.22%. The TER can, of course, be checked on our website.

Higher costs of European ETFs result from more extensive regulations (UCITS), smaller market scale, higher distribution costs, and lower competitiveness compared to the USA.

ETF costs in the USA

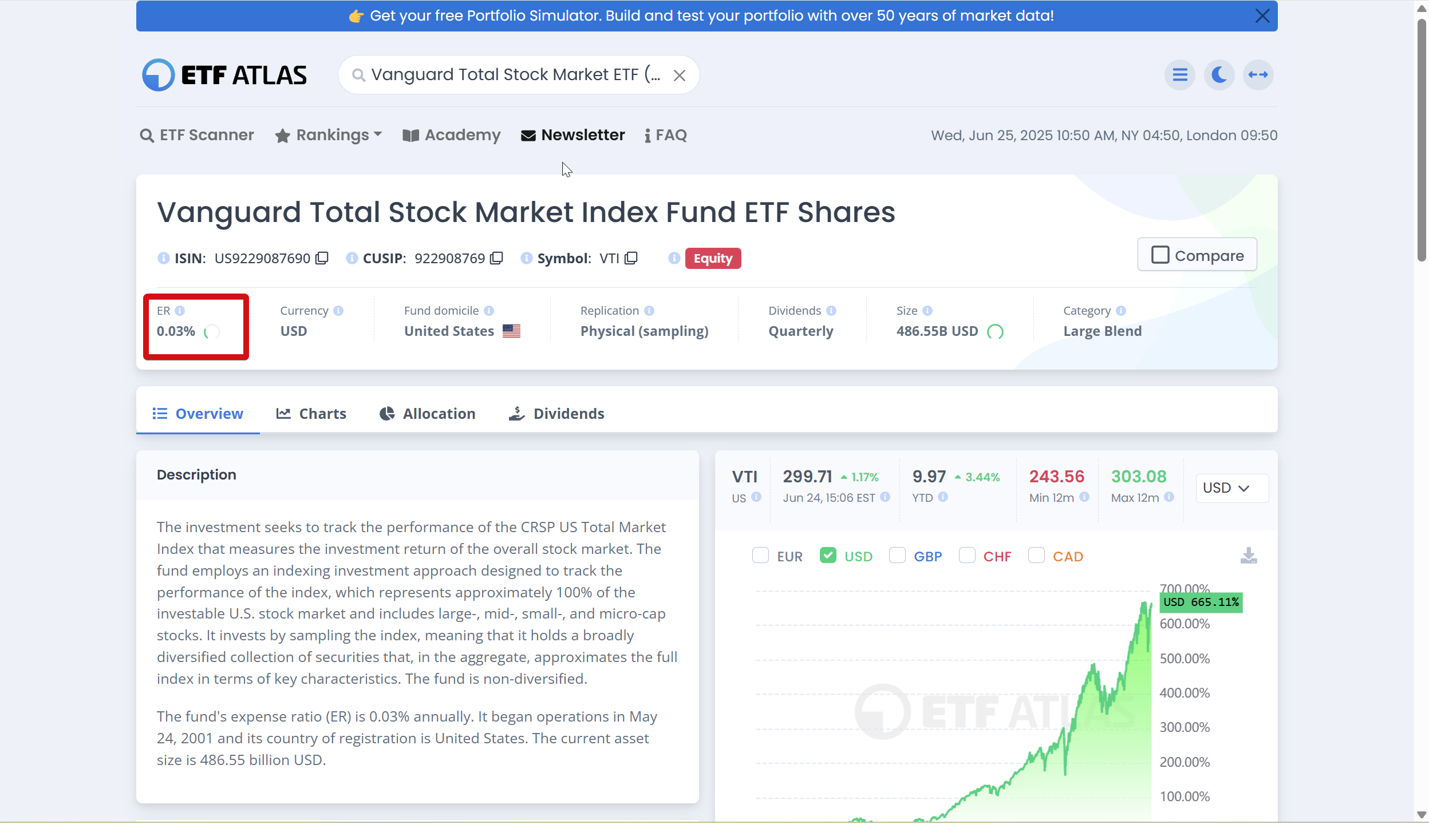

In the United States, ETFs are generally cheaper than their European counterparts. The average TER for American index ETFs is about 0.05–0.10%, and the cheapest funds, such as Vanguard Total Stock Market ETF (VTI), have management costs as low as 0.03%. Even more complex ETFs rarely exceed 0.2–0.3%.

Lower costs in the USA are due to larger market scale, greater competition, simplified regulations, and the fact that many ETFs are used in retirement plans, allowing for lower negotiated fees.

In Europe, the term TER (Total Expense Ratio) is standard, while in the USA, ER (Expense Ratio) is used. Both indicators mean practically the same thing – the percentage value of all fixed ETF management costs annually, including management, administration, accounting, or index license fees.

European fund documents may also use the term OCF (Ongoing Charges Figure), which is equivalent to TER and also includes all ongoing fund fees. In practice, TER, ER, and OCF are very similar in scope and meaning but differ in name depending on the region and reporting standards.

In conclusion, ETFs are investment instruments combining transparency, low costs, and broad accessibility, making them an attractive choice for various types of investors. The features discussed in the article, such as domicile, ISIN, strategy, currency, hedging, dividend policy, replication method, listing markets, ticker, asset size, or management costs, allow for an informed choice of the fund best suited to individual needs and investment strategy. For more practical information, visit etfatlas.com – where you can find everything necessary to navigate the world of ETFs effectively.