Physical replication is the simplest and most common way ETFs track an index. But don’t overlook the synthetic method. Sometimes it’s the only way to get into certain markets, and it can even bring better returns. In this video, you’ll find out how these replication methods differ, how synthetic replication actually works, and whether it’s worth using.

What are the types of replication?

Exchange-traded funds, or ETFs, were made to follow indexes. Sure, there are now lots of actively managed ETFs that don’t track any index, but mostly, ETFs still stick to index strategies. And while index investing can be active too, figuring out where passive ends and active begins is a topic for another discussion.

So how does an ETF follow an index? There are a few main ways, called “replication methods”:

- Full physical replication

- Partial physical replication (sampling)

- Synthetic replication

- Hybrid replication

Full physical replication means the fund buys every single stock in the index, in the right amounts. This works best for indexes with fewer companies, like the Nasdaq-100.

Partial physical replication (sampling) means buying a selected subset of companies from the index to represent the entire index. It is commonly applied to indexes with many constituents, like MSCI ACWI, which has about 2,500 positions.

The synthetic method uses derivatives, most often swap contracts. It is used when other methods are difficult, costly, or simply impossible. This approach allows access to hard-to-reach markets or reduces costs.

The hybrid method mixes physical and synthetic approaches. For example, the Scalable MSCI AC World Xtrackers UCITS ETF replicates part of its portfolio physically and part synthetically, choosing the most efficient method for each part of the index.

On ETFatlas.com you can filter ETFs by replication method. Just use the “Replication” filter in the ETF Scanner on the left side. To decide whether to prefer one method over another, it’s useful to examine funds that use different replication techniques.

How often do funds use each replication method?

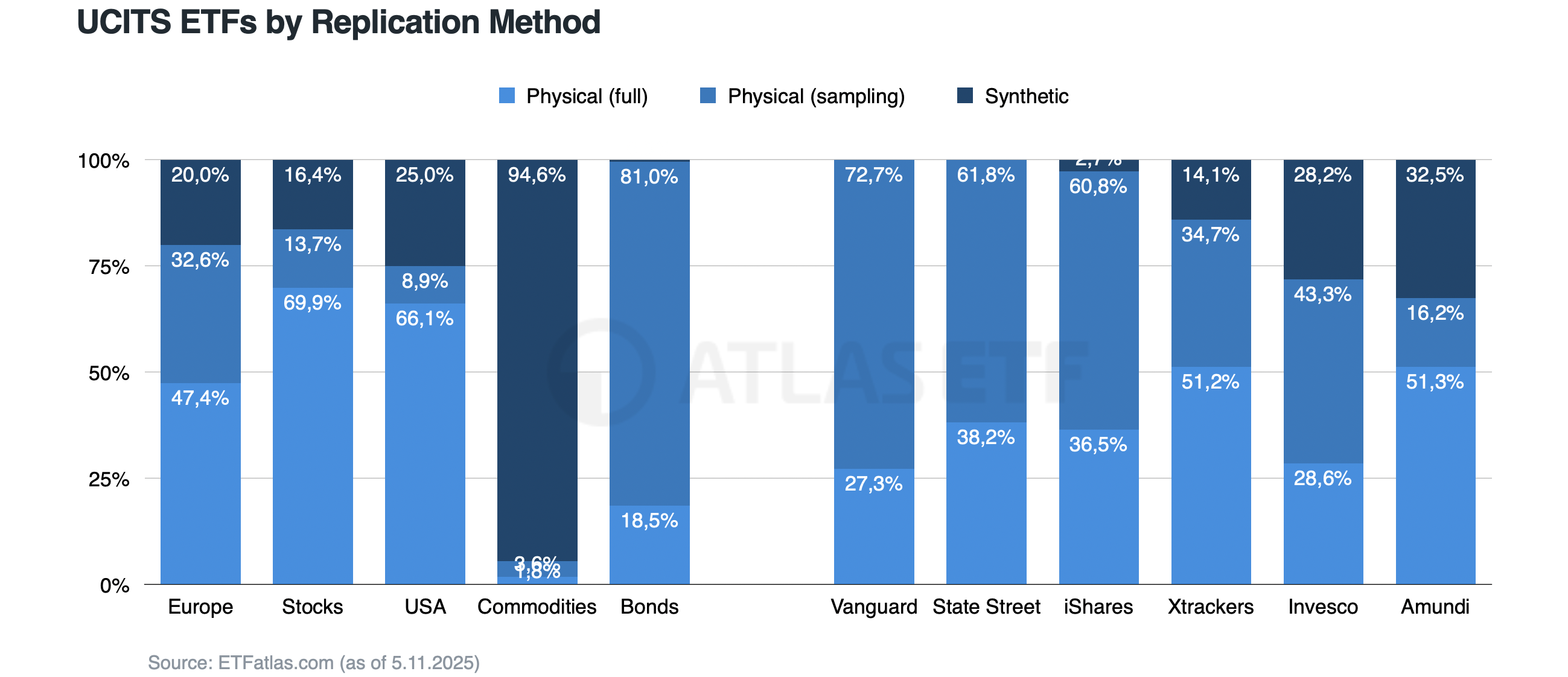

In the US, almost all ETFs use physical replication. Since 2010, US law basically doesn’t allow synthetic replication. The only exception is for leveraged ETFs, like ProShares UltraPro QQQ.

Synthetic replication is mainly used by funds governed by European Union law (UCITS). It is used by about 20% of these funds (data as of November 5, 2025). This method is particularly popular in commodity funds, where physical asset storage is problematic, and in equity funds—especially American equities—where roughly 25% of funds use synthetic replication. Among bond funds, synthetic replication is very rare (about 0.5%).

Although synthetic replication is allowed in Europe, not all providers use it. For example, Vanguard and State Street avoid it, and iShares only use it a little. The main users are companies like Amundi, Invesco, and Xtrackers. Although synthetic funds represent a minority share of their portfolios.

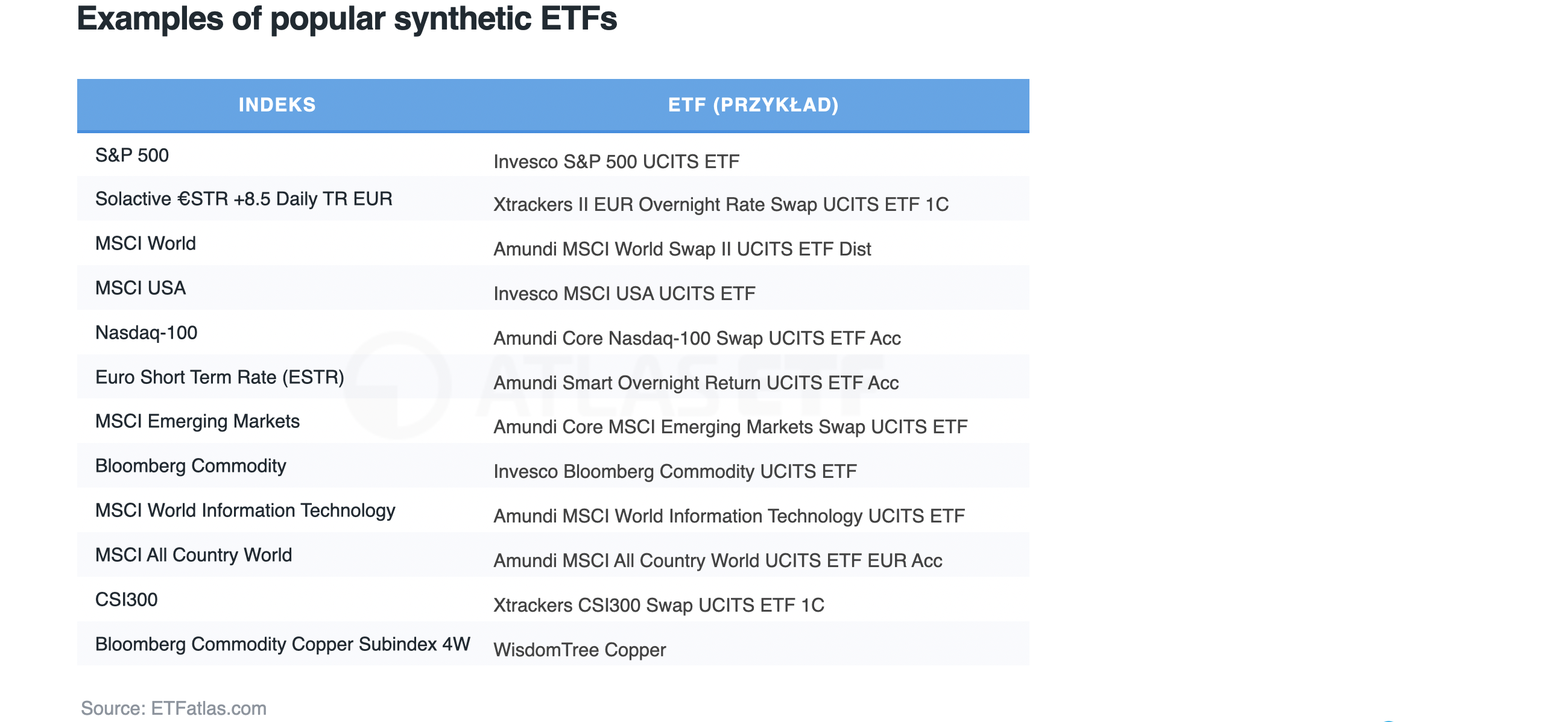

The largest synthetic ETFs mostly track US equity indexes like the S&P 500, MSCI USA, and Nasdaq-100, as well as global indexes such as MSCI World and MSCI ACWI. But there are also funds focused on emerging markets (like MSCI Emerging Markets index) and on the euro short-term interest rate (Euro Short Term Rate).

Which replication type to choose?

Sometimes synthetic replication is the only way to get exposure to a particular market or index, like commodities or the euro short-term interest rate. However, more often, funds using different replication methods are available for the same market. Which method delivers better results? Analysis shows synthetic replication does not generally outperform. Take MSCI Emerging Markets ETFs as an example—synthetic funds have not delivered better returns. Results have been similar over various periods. So it is best to follow the principle “invest in what you understand” and prefer the physical replication method, which is simpler.

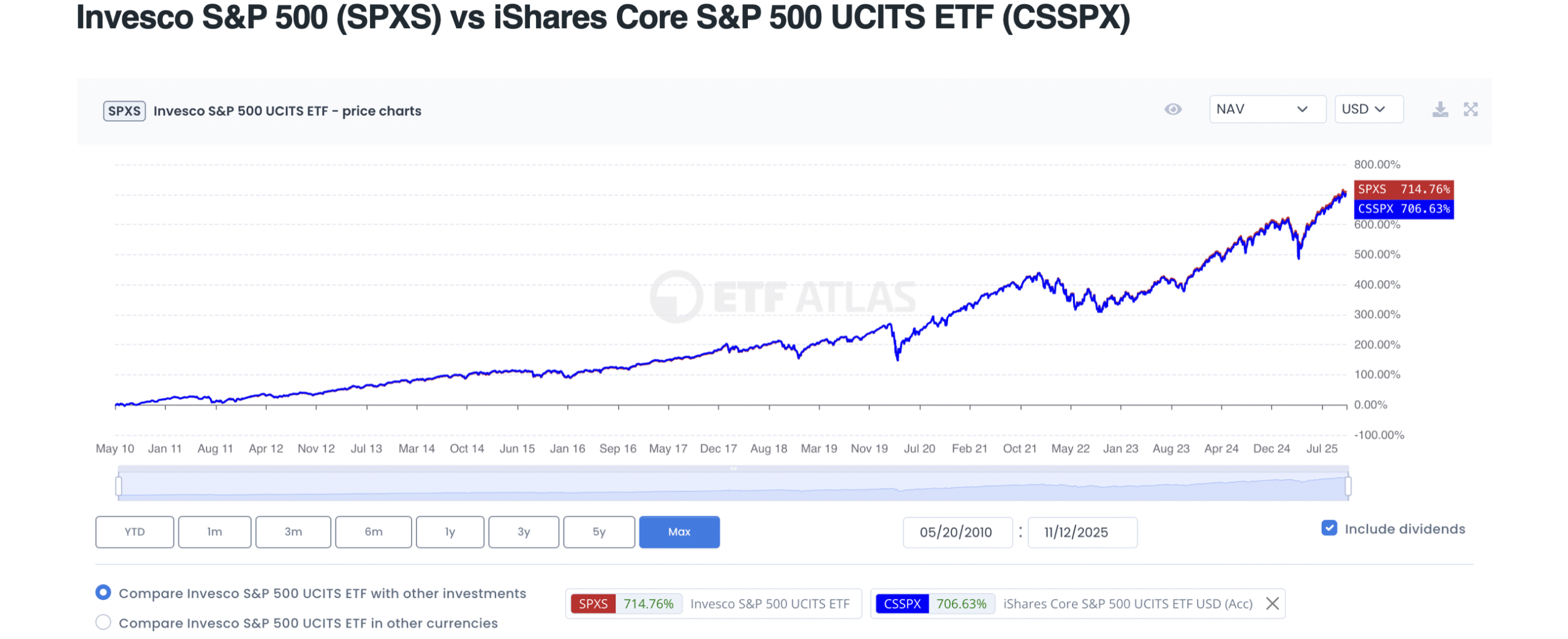

However, synthetic replication can sometimes offer an advantage. A good example of such exception is US equities, which are among the most popular investment options. The S&P 500, Nasdaq-100, and MSCI USA are some of the best-known indexes worldwide, and ETFs tracking them hold some of the largest assets. In this case, synthetic replication allows investors to legally avoid the US withholding tax on dividends. As a result, synthetic ETFs often deliver higher returns than physical ones. For example, the synthetic Invesco S&P 500 UCITS ETF outperformed the physical iShares Core S&P 500 UCITS ETF USD (Acc) by 0.2 percentage points over the last year, 2 percentage points over five years, and 8 percentage points over 15 years.

However, in investing, there are no free lunches. The higher returns come with counterparty risk. In 2017, the Federal Reserve stated clearly that synthetic ETFs involve greater risk than physical ETFs because investors face counterparty risk.

Since then, many safeguards have been introduced to reduce this risk. Choosing synthetic replication should depend on how well you understand it and whether you think potentially higher returns are worth the risk.

How does synthetic replication work?

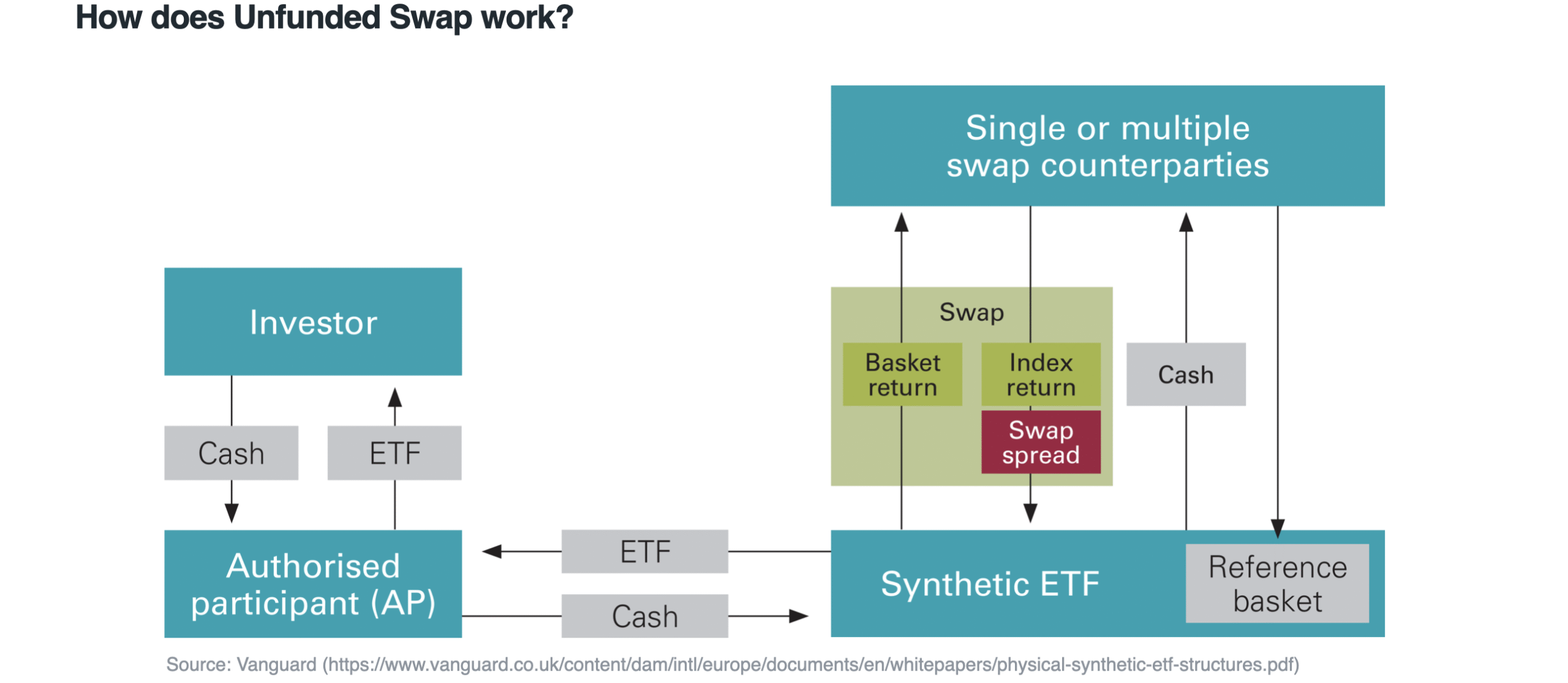

Synthetic replication uses swap contracts between the ETF and a counterparty—usually a large and stable financial institution, like an investment bank. There are theoretically two types of swaps: Funded Swap and Unfunded Swap. But Funded Swaps are already almost a history. In most cases, ETFs use Unfunded Swaps. In short, the fund transfers cash to the counterparty and receives the return of the chosen index in exchange. This contract is secured by a portfolio of liquid financial instruments (called collateral), which become the property of the fund if the counterparty fails, limiting counterparty risk.

Counterparties are generally large, stable institutions, providing a sense of security. However, history knows failures of big institutions—like Lehman Brothers in 2008. If a counterparty goes bankrupt, does the fund lose everything and investors lose money? No, because collateral is put in place to protect against situations like that. In the case of bankruptcy, the collateral is transferred to the ETF.

Does the collateral contain the same instruments as the tracked index? No. And this is the counterparty risk. In case of counterparty bankruptcy, the fund may end up with a collateral package different from the index it replicates. It can cause a mismatch and result in value loss. However, it’s worth noting that these are usually liquid instruments, such as US stocks or bonds.

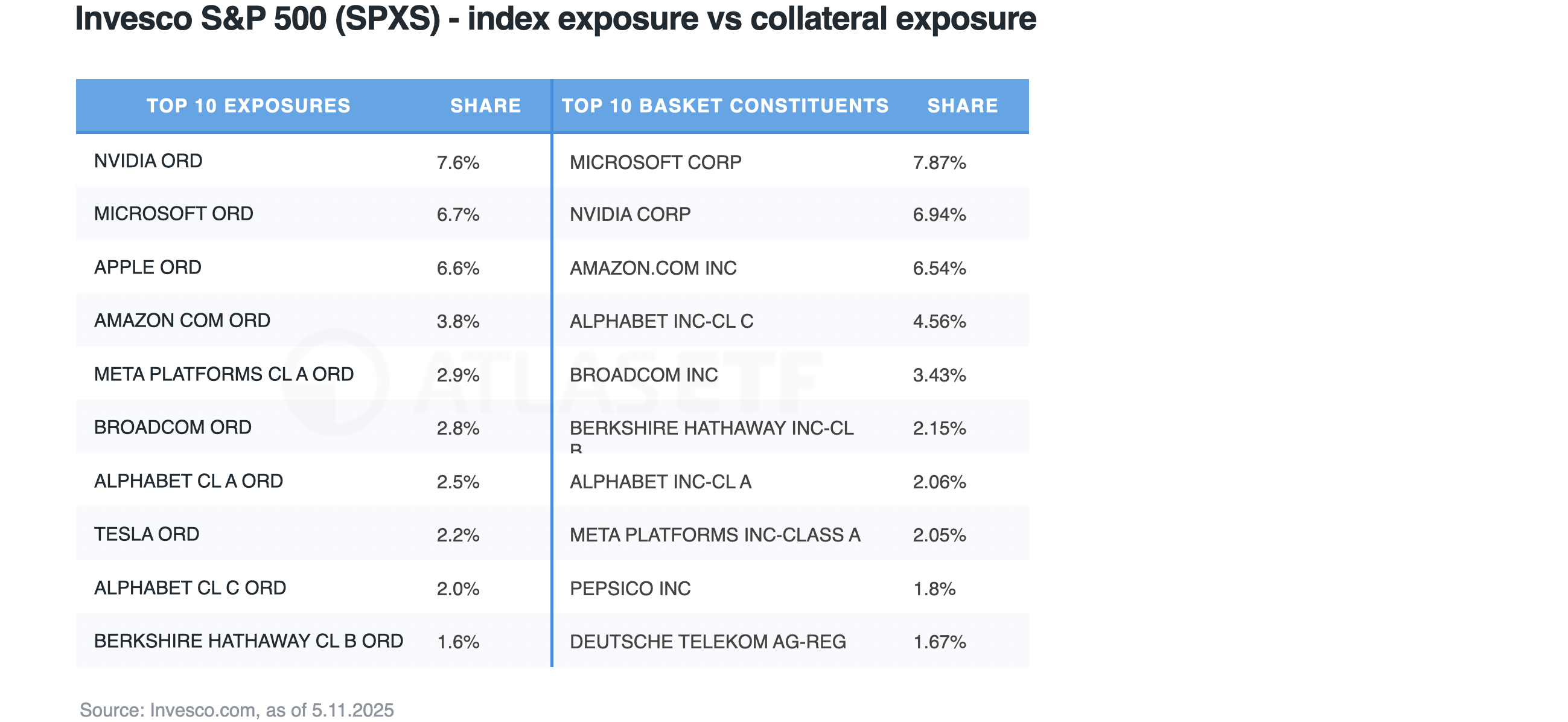

Take the Invesco S&P 500 UCITS ETF example and look at the top 10 holdings. The collateral composition is similar to the index but differs in weightings. The mismatch difference appears very small. This might explain why even conservative iShares launched a synthetic US equity ETF in 2020—the iShares S&P 500 Swap UCITS ETF USD (Acc).

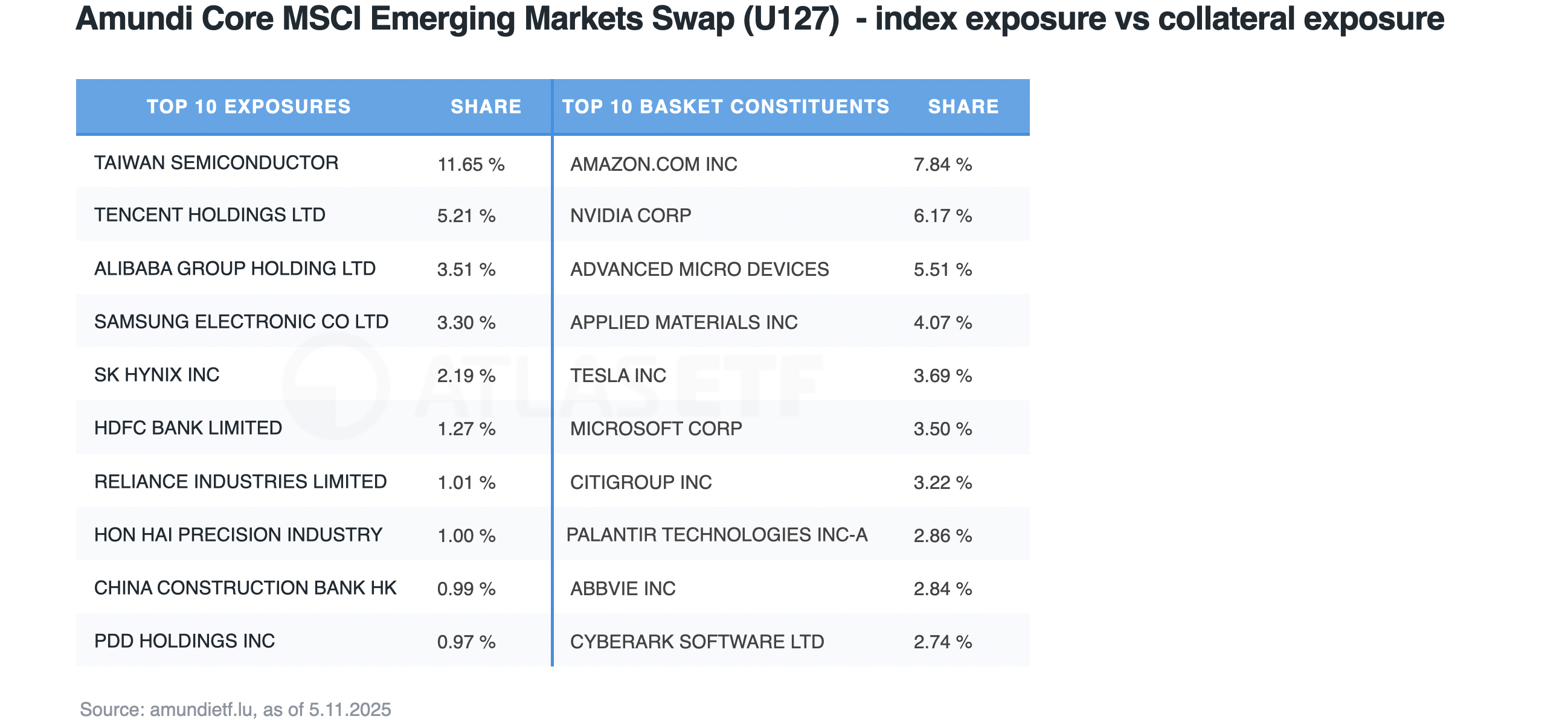

But it can also look different. In the Amundi Core MSCI Emerging Markets, the portfolio contains emerging market shares, while the collateral holds US stocks. This can lead to differences in valuation.

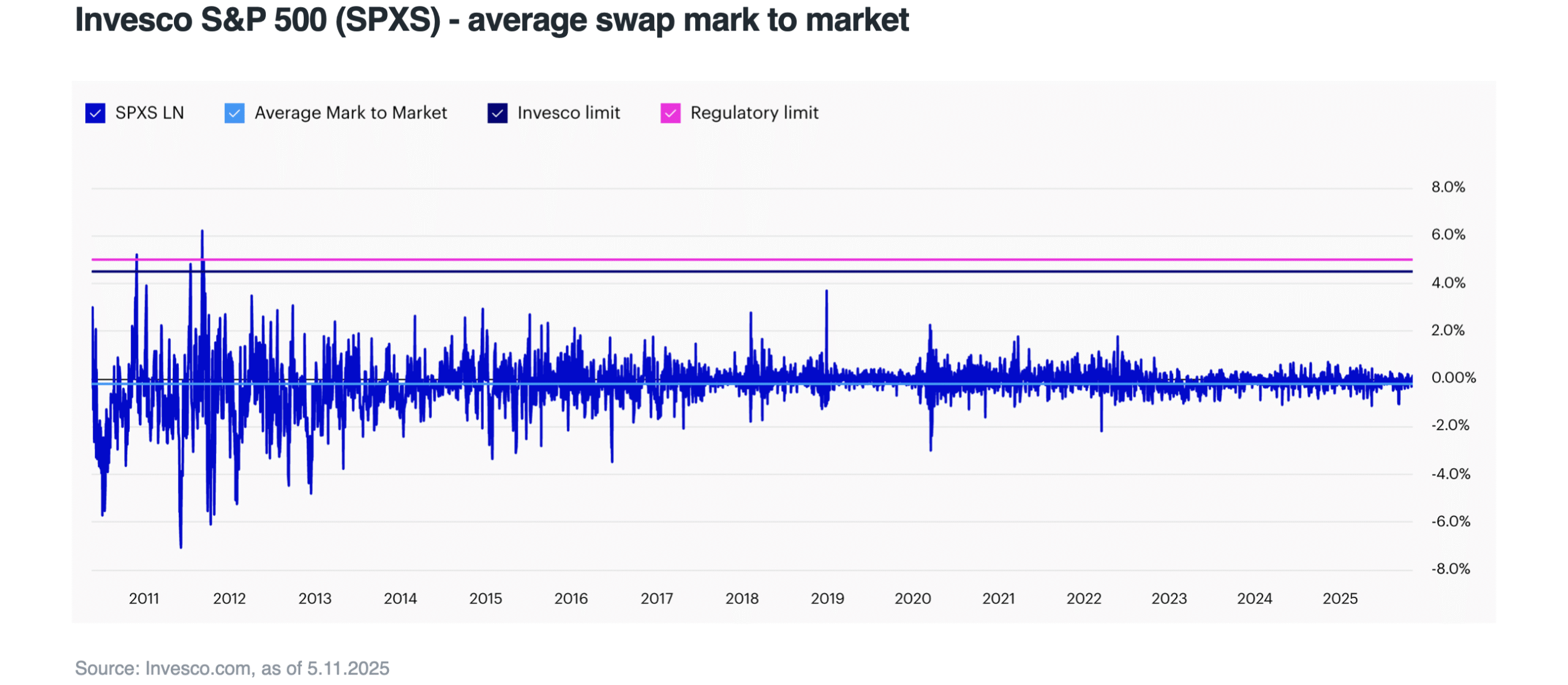

What if the counterparty goes bankrupt and the collateral’s value drops below the index portfolio’s value? Will investors lose money? Yes, this is the essence of counterparty risk. But over recent years, much has been done to limit this risk. EU law requires collateral value never drop below 90% of the swap contract value, with daily mark-to-market valuation. In practice, collateral is usually overcollateralized. For example, the average mark-to-market ratio for the Invesco S&P 500 (SPXS) is slightly negative (-0.21), meaning the fund is overcollateralized, reducing counterparty risk and increasing investor safety.

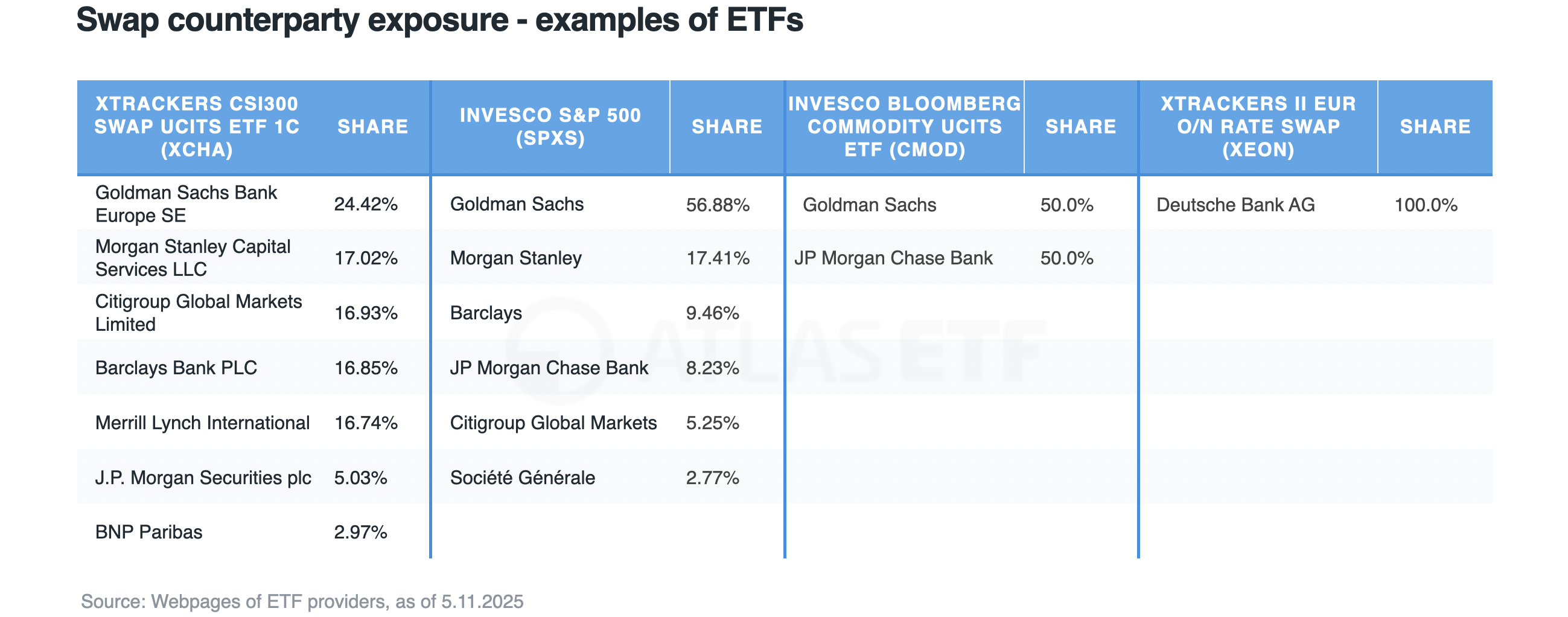

Additionally, funds often have swap contracts with multiple counterparties, which diversifies risk. For example, Xtrackers CSI300 (XCHA) works with seven counterparties, and Invesco S&P 500 (SPXS) with six. The number may depend on the asset class. Xtrackers II EUR O/N Rate Swap (XEON) has mostly very liquid US bonds as collateral, so a single counterparty contract may be sufficient.

Finally, there’s also liquidity risk. If a counterparty fails and collateral is taken over, the fund will try to liquidate it and buy index assets. If the collateral portfolio is large, this process could affect prices of the underlying assets, creating liquidity risk.

Summary

There are three main ETF replication methods: full physical, partial physical (sampling), and synthetic. Physical replication is the simplest and most commonly used by funds, and following “invest in what you understand” it should be the default choice for most investors. Synthetic replication does not necessarily generate better results, so it should not be preferred automatically. Yet, it should not be dismissed either, as it is often the only option to access some markets, and for US equities it can offer tax advantages.

Synthetic replication carries counterparty risk, which is now minimized by regulations and safeguards (e.g., maintaining collateral at at least 90% of swap value, and diversifying counterparties). Investors should assess if they are willing to accept this risk for potentially higher returns.

Also, note that physical replication funds can have counterparty risk too—in situations involving securities lending, which are secured by guarantees. Although this risk is usually small, it differs in nature from synthetic replication risk but is still present.